What’s Ahead:

- “Perfect” can be the enemy of “good” when it comes to building and maintaining the right financial plan — even for the most emotionally stable clients.

- Fear and greed are the animal spirits that can lead investors down dangerous roads — this rings true across the investor and market-environment spectrums.

- Protective investment solutions promote what behavioral economists call “the IKEA effect,” and its benefits can be seen in bull, bear, and boring markets.

There’s a never-ending supply of hot new investment ideas flooding advisors’ inboxes. Some of them are legit, grounded in empirical evidence with robust back-tested success. Many indeed have merit; today’s technology streamlines transaction processes and lowers costs for the retail investor, just as recent innovations in financial engineering are truly something to behold when applied the right way.

We know. Halo has been pioneering the protective investment space for years, helping to bring Structured Notes, annuities, and buffered ETFs to the mass-affluent crowd through RIAs and advisors at larger brokerage houses.

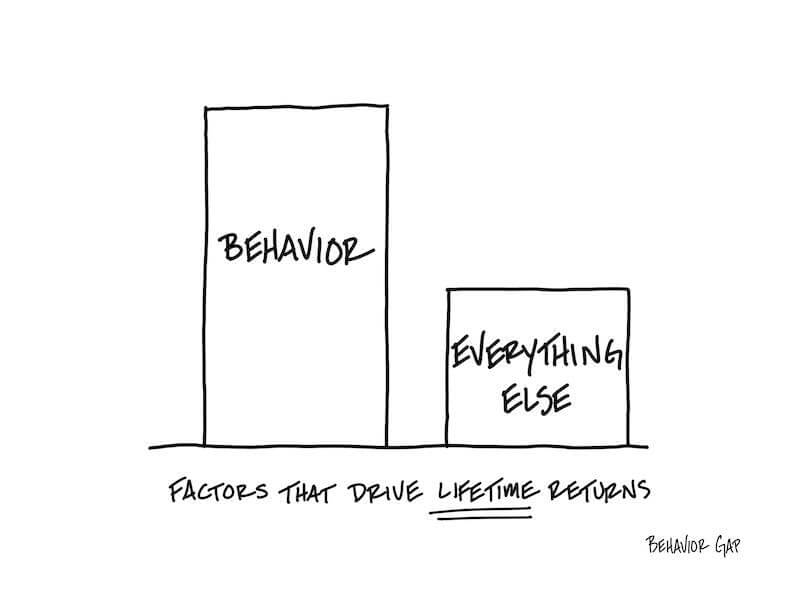

Behavior Above All Else

We must admit, however, that one factor trumps all others when it comes to helping individual investors reach their financial goals: behavior. After all, the most stress-tested, scenario-analysis successful, and weathered portfolio means nothing if Joe and Jane Investor cannot stick with it through the good times — and the bad. So, as you sift through that jammed inbox of yours, fraught with noise and pitchmen waving their signboards at you to buy into a hot new strategy, always remember that the biggest x-factor in the alpha-generating formula is what your clients will do when volatile bear markets strike, when periods of calm endure, or when euphoria conjures up greedy animal spirits.

Park Yourself on the Proverbial Money Couch

That leads us to wonder: What kind of portfolio would be most resistant to veering off course amid the ups and downs of Wall Street’s unpredictable journey? We can refer to behavioral economics to find out. Yes, during wild times in financial markets, Danny Kahneman, Richard Thaler, and Morgan Housel (among others) can be the go-to experts for us to find rational answers to irrational situations.

Building a Financial Plan: Leveraging the IKEA Effect for Client Engagement

In one of our most popular Journal articles, we touched on how the IKEA effect can be harnessed, but let’s dive deeper here. The IKEA effect is a cognitive bias that suggests people tend to place a higher value on products or outcomes in which they have invested their personal effort, time, or resources. By understanding this mental quirk, financial advisors can employ strategies to foster client engagement and commitment. This promotes a team-like setting as you and your client not only build a financial plan (which is arguably easier and more fun than piecing together a chic bed frame from IKEA) but also set an investment plan into motion.

“Yeah, I built that” is how the client might feel, even though you, as advisor, did all the work. The key aspect here is that by actively engaging your clients and allowing them to contribute to the decision-making process, they develop a sense of ownership and attachment to the plan. The upshot: They may be less prone to acting emotionally during shaky times in the market.

Volatile Markets and Misbehaving Investors: Smoothing Out the Roller-Coaster Ride

On that note, our team finds that volatile markets get all the press as it pertains to retail investors misbehaving with their money. We are guilty as charged here! Volatility can truly inflict pain on risk-conscious investors’ financial plans, so it’s nothing to throw shade on. To bring down a portfolio’s standard deviation, including protective investments like Structured Notes, the right type of annuity, or a low-cost buffered ETF can certainly help buttress a traditional allocation mix. However, the last few years have brought about a range of markets, not just intense bear-market price action.

From Relief to Euphoria: Managing the Siren Songs of Speculative Booms

Consider the period between the third quarter of 2020 through 2021. That stretch was initially one of relief but also anxiety-riddled as fears of another major COVID-19 outbreak undermined the S&P 500’s recovery. Eventually, though, confidence began to grow, and backstops provided by global central banks along with unprecedented fiscal stimulus drew Wall Street’s bulls out of a deep sleep. Euphoria burst onto the scene in late 2020. The IPO market was hot, SPACs surged (few market participants even knew what these were), meme mania broke out, and day traders trolled TikTok.

While much ink was spilled elucidating bear markets and investor behavior, extreme frothiness can impair judgment just as much. The IKEA effect reveals its value during those periods, too. A carefully crafted strategy implemented by you and your client can help reduce the FOMO risk. Though it is not an elixir for the temptation of climbing aboard a hot product promising quick profits, a tailored plan does help reduce herd behavior.

Calm and Boring Markets: The Hidden Dangers of Complacency and How to Stay on Track

Shifting gears, now let’s turn to the rarely talked about calm, low-VIX, and straight-up boring style of markets. “Surely, those can’t be all that treacherous,” you might say, but there were more nuanced pitfalls at play during periods like 2013 and 2017 when bull markets thrived and greediness felt tempered. Investors may have become complacent and overly confident, lulling themselves into a false sense of security. At times like these, it becomes all too easy to stray from a risk management plan. Investors might dabble in pet projects and opaque alternative products that not only harm their returns but also negatively twist their psyche.

During these times, it’s key to regularly review the plan you and the client constructed, do the usual rebalancing with an asset allocation update, and get a refresh on the client’s money values to help pin down specific goals. All of these activities underscore the point of long-term investing and will help to keep them on the right money journey.

The Bottom Line

Halo’s protective investment solutions can help improve the quantitative metrics of an investor’s allocation, but they also help promote client engagement, which can help clients lean into a durable financial plan. The sense of personal involvement and attachment to a chosen strategy, coupled with the potential financial benefits offered by Structured Notes, annuities, and defined outcome funds, can help everyday investors stay the course, avoid impulsive decisions (during bull markets, bear markets, and boring markets), and ultimately get them to hit their financial goals sooner.

Annuities are not suitable for all investors. All recommendations for annuity products must be suitable and appropriate for the client and must be based on a thorough fact finding and understanding of the client’s unique financial situation, needs, goals, and risk tolerance.

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Buffered ETFs’ are different from more typical investment products, and the funds may be unsuitable for some investors. It is important that investors understand the investment strategy before making an investment. Investment involves risk, including possible loss of principal. There is no guarantee the funds will achieve their investment objectives.

Please see our Halo Disclosure Page for important disclosures.