Rethinking Modern Asset Allocation: A Framework for Structured Notes

Looking to improve risk-adjusted outcomes without resorting to overly complex or illiquid alternative investments?

Structured Notes may offer a compelling solution — a versatile tool that may enhance traditional portfolios.

")

–

But how?

When complementing existing asset allocation frameworks, Structured Notes make it possible to build portfolios using tried-and-tested risk management techniques with similar risk characteristics to traditional portfolios, but with the potential for improved returns.

More specifically, Structured Notes can position the efficient frontier for a “Z-shift.”

Why Advisors Like Structured Notes for Portfolio Enhancement

New sources

of diversification

Potential

for alpha generation

asset classes

Visualizing How Structured Notes Can Tilt Investment Outcomes in Your Favor

You’re probably familiar with the traditional distribution, where returns follow a “normal,” bell-curved pattern. However, seeing that markets tend to go through periods of bullish and bearish cycles, different return patterns are just as likely.

For an aggregate portfolio, tilting it to take advantage of a bullish or bearish point of view (asymmetry) can be challenging, particularly without disrupting policy portfolio positioning or inviting tracking errors.

Structured Notes, however, can be structured to take advantage of unique market outlooks or specific asset class points of view. For example, a Note can be designed to outperform its underlier if markets trend bearish. Or vice versa if markets have a greater likelihood of ending higher. By concentrating investment outcomes to their highest probabilities, structured investments can help investors shape a return distribution to their most desired profile. This is why they’re called defined-outcome investments.

Structured Notes, however, can be structured to take advantage of unique market outlooks or specific asset class points of view. For example, a Note can be designed to outperform its underlier if markets trend bearish. Or vice versa if markets have a greater likelihood of ending higher. By concentrating investment outcomes to their highest probabilities, structured investments can help investors shape a return distribution to their most desired profile. This is why they’re called defined-outcome investments.

Implementing a Structured Note Asset Allocation Framework

To add Structured Notes to portfolios, our framework utilizes a three-step process.

Identify investment

or portfolio challenge

Begin by identifying your investment or portfolio challenge. For example, this could include inadequate investment income available in conventional fixed income instruments, or sequence

of return risk for an investor nearing retirement or the decumulation phase.

Determining the issue to be addressed by a Structured Note is essential to setting up Step 2, selecting a Note’s features.

Hedge equities

- When equity returns lead to lofty valuations or to manage risk due to market/economic conditions

- Retain upside return potential

- Reduce downside risk

Alternative to Alts

- When alternatives in a portfolio aren’t performing or are difficult to track and manage

- Add differentiated sources of return

- Add specific risk targets

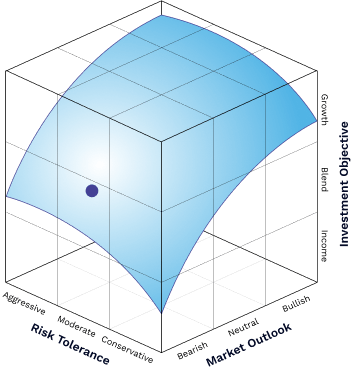

Align Note Features with Investment

Objective, Market Outlook, and

Protection Level(s)

Structured Notes begin to shine in the second step. Here, Notes are selected for their unique attributes. These could include an emphasis on above-market yields or a structure that outperforms in flat markets. Or perhaps, additional downside protection is desired.

By taking advantage of the flexibility available in Structured Notes, investors can leverage portfolio construction techniques often unavailable in conventional asset allocation approaches or once limited to high-net-worth and institutional investors.

Source: Halo Investing. For illustrative purposes only

Funding an Allocation

to Structured Notes

Funding an allocation to Structured Notes is straightforward. Generally, advisors pull from equities, fixed income, or alternative investments.

However, specific portfolio objectives requiring a more precise allocation and funding strategy could arise. For instance, an investor may want to reduce specific risks, such as equity, longevity, or duration.

Our framework features two funding strategies:

The layered approach:

Structured Notes are layered on top of existing asset allocations. For example, a Note linked to the S&P 500 shouldn’t be viewed as a replacement or substitute, but rather, a complementary allocation to an existing exposure.

The replacement strategy:

To shift a portfolio’s exposure from one asset class to another, a replacement approach is a direct way to fund a new allocation to Structured Notes.

Layered in addition to existing asset allocations

Take the place

of existing asset allocations

Source: Halo Investing. For illustrative purposes only.

Implementing a Structured Note Asset Allocation Framework

To add Structured Notes to portfolios, our framework utilizes a three-step process.

Step 1

Identify investment

or portfolio challenge

Begin by identifying your investment or portfolio challenge. For example, this could include inadequate investment income available in conventional fixed income instruments, or sequence

of return risk for an investor nearing retirement or the decumulation phase.

Determining the issue to be addressed by a Structured Note is essential to setting up Step 2, selecting a Note’s features.

Hedge equities

- When equity returns lead to lofty valuations or to manage risk due to market/economic conditions

- Retain upside return potential

- Reduce downside risk

Alternative to Alts

- When alternatives in a portfolio aren’t performing or are difficult to track and manage

- Add differentiated sources of return

- Add specific risk targets

Align Note Features with Investment Objective, Market Outlook, and Protection Level(s)

Structured Notes begin to shine in the second step. Here, Notes are selected for their unique attributes. These could include an emphasis on above-market yields or a structure that outperforms in flat markets. Or perhaps, additional downside protection is desired.

By taking advantage of the flexibility available in Structured Notes, investors can leverage portfolio construction techniques often unavailable in conventional asset allocation approaches or once limited to high-net-worth and institutional investors.

Source: Halo Investing. For illustrative purposes only

Funding an Allocation

to Structured Notes

Funding an allocation to Structured Notes is straightforward. Generally, advisors pull from equities, fixed income, or alternative investments.

However, specific portfolio objectives requiring a more precise allocation and funding strategy could arise. For instance, an investor may want to reduce specific risks, such as equity, longevity, or duration.

Our framework features two funding strategies:

The layered approach:

Structured Notes are layered on top of existing asset allocations. For example, a Note linked to the S&P 500 shouldn’t be viewed as a replacement or substitute, but rather, a complementary allocation to an existing exposure.

The replacement strategy:

To shift a portfolio’s exposure from one asset class to another, a replacement approach is a direct way to fund a new allocation to Structured Notes.

Layered in addition to existing asset allocations

Take the place

of existing asset allocations

Source: Halo Investing. For illustrative purposes only.

Seeing the Framework in Action

CASE STUDY

Enhancing the 60/40 portfolio

with Structured Notes

To illustrate the Framework’s potential, we’ll look to enhance the classic 60/40 portfolio with Structured Notes.

For this example, rather than dipping into the uncertainties of private and alternative asset classes to improve the portfolio, we’ll retain core exposure to stocks and bonds and allocate 10% of a portfolio’s equity sleeve to a Growth Note, while 10% of fixed income is reallocated to an Income Note.

Exhibit 1 presents performance and risk statistics for a “60/40” portfolio with and without Structured Notes. We see Structured Notes improve the classic “60/40” portfolio on a risk-adjusted basis when considering both Sharpe and Sortino ratios.

Overall, as expected, the portfolio enhanced with Structured Notes behaves similarly to the classic “60/40” portfolio. For example, both portfolios share similar projected max drawdowns and negative return frequencies.

The diversification benefits are most obvious when looking at up/down capture: The portfolio enhanced with Notes is projected to capture 118% of the classic ”60/40” upside but only 14% of its downside.

This effect is more obvious in Exhibit 2, where we see Notes improving the efficient frontier by moving it up and to the left. With returns and risk lining up almost linearly for the classic “60/40,” defined-outcome strategies provide investors with a vehicle to fine-tune to a desired risk-and-return profile in terms of market exposure with higher risk-adjusted returns than in a traditional portfolio with no structured investments.

A Modern Framework

for Portfolio Personalization

To see the entire white paper and learn where Structured Notes fit in a portfolio, download today

")

Personalization

The framework features a unique approach to integrating both client and advisor objectives and points of view.

Improved Investment Outcomes

The framework, while simple in setup, has the potential to improve risk-adjusted results across multiple fronts. Particularly, downside risk mitigation.

Enhanced Investment Experience

The framework has the potential to improve the overall investment experience by creating a smoother ride for investors.

Ready to Take Your Portfolio Analysis to the Next Level? Introducing Aura, by Halo Investing

Aura is the first simulation tool built specifically to model the role of Structured Notes in portfolio construction. Integrated directly into the Halo platform, Aura helps advisors quantify Structured Note allocations, visualize their potential impact, and clearly communicate investment strategies to clients.

")

Important Disclosure

The results are hypothetical and derived from a Monte Carlo simulation, are not an indicator of future results, and do not represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged and do not reflect management or trading fees. One cannot invest directly in an index.

Monte Carlo simulations model future uncertainty. In contrast to tools generating average outcomes, Monte Carlo analyses produce outcome ranges based on probability—thus incorporating future uncertainty.

Material assumptions

- Multiple capital market assumptions were used in the analysis to assess the performance of hypothetical products under different market environments. Material limitations include: Users should also keep in mind that seemingly small changes in input parameters, including the initial values for the underlying factors, may have a significant impact on results, and this (as well as mere passage of time) may lead to considerable variation in results for repeat users.

Material limitations

- The analysis relies on assumptions, combined with a return model that generates a wide range of possible return scenarios from these assumptions. Despite our best efforts, there is no certainty that the assumptions and the model will accurately predict asset class return ranges going forward. As a consequence, the results of the analysis should be viewed as approximations, and users should allow a margin for error and not place too much reliance on the apparent precision of the results.

- Users should also keep in mind that seemingly small changes in input parameters, including the initial values for the underlying factors, may have a significant impact on results, and this (as well as mere passage of time) may lead to considerable variation in results for repeat users.

- Extreme market movements may occur more often than in the model.

- Market crises can cause asset classes to perform similarly, lowering the accuracy of our projected return assumptions and diminishing the benefits of diversification (that is, of using many different asset classes) in ways not captured by the analysis. As a result, returns actually experienced by the investor may be more volatile than projected in our analysis.

- The analysis does not use all asset classes. Other asset classes may be similar or superior to those used.

- Not all fees and transaction costs are not taken into account. Outcomes illustrated could differ if fees associated with actual investing were assumed.

- The analysis models asset classes, not investment products. As a result, the actual experience of an investor in a given investment product may differ from the range of projections generated by the simulation, even if the broad asset allocation of the investment product is similar to the one being modeled. Possible reasons for divergence include, but are not limited to, active management by the manager of the investment product. Active management for any particular investment product—the selection of a portfolio of individual securities that differs from the broad asset classes modeled in this analysis—can lead to the investment product having higher or lower returns than the range of projections in this analysis.

Modeling assumptions

- The primary asset classes used for this analysis are stocks and bonds. An effectively diversified portfolio theoretically involves all investable asset classes including stocks, bonds, real estate, foreign investments, commodities, precious metals, currencies, and others. Since it is unlikely that investors will own all of these assets, we selected the ones we believed to be the most appropriate for long‑term investors.

- The analysis includes 10,000 simulated scenarios for each asset class analyzed.

- IMPORTANT: The projections or other information generated by Halo Investing regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. The simulations are based on assumptions. There can be no assurance that the projected or simulated results will be achieved or sustained. The charts present only a range of possible outcomes. Actual results will vary with each use and over time, and such results may be better or worse than the simulated scenarios. Clients should be aware that the potential for loss (or gain) may be greater than demonstrated in the simulations.

- The results are not predictions, but they should be viewed as reasonable estimates.

The content provided by Halo Investing is for educational purposes only. This information neither is, nor should be construed, as an offer, or a solicitation to sell or solicitation of an offer to buy securities. It is the responsibility of the financial professional viewing this to understand and evaluate any prospective investment. Such considerations shall be based on a review of applicable offering documents, an evaluation of client financial circumstances, investment objectives, risk tolerance, liquidity needs, and any features of the specific structured note product.

The opinions expressed herein do not take into account individual client circumstances, objectives, or needs and are therefore not intended to serve as investment recommendations. No determination has been made regarding the suitability of particular strategies to particular clients or prospects. The financial indices referenced herein is provided for informational purposes only. You cannot invest directly in an index. The statistical data regarding such indices has been obtained from sources believed to be reliable but has not been independently verified.

Investors should be aware that there is often a cost to purchasing options (premium) to achieve leveraged returns with structured notes. In aggregate, that cost is reflected in structured note returns. Investors should be aware that structured notes do not capture returns from dividends on the underlying index. For example, the S&P 500 Index does not include dividends whereas an S&P 500 Index fund pays dividends (thus it is a total return product that captures both price returns and dividend income). The return difference between the S&P 500 Index, on which a structured note might be priced, and funds tracking it will grow larger (in favor of the funds) over time. Investors should be aware that structured notes have counterparty risk, and therefore, should require a higher return to be equivalent to an index fund on a risk-adjusted basis. Structured note pricing should include a risk premium to compensate investors for that added risk. Investors should be aware that structured notes have finite terms. An added burden and risk structured note holders face is reinvesting proceeds at maturity.

Investors should be aware that structured notes are less liquid than heavily traded exchange-traded funds (ETFs). Moreover, most mutual funds can be redeemed at Net Asset Value (NAV) each day. Investors are generally not compensated for reduced liquidity in structured products. Structured notes should be priced to account for their relative lack of liquidity. The notes referenced herein are for illustrative purposes. Other notes may or will have different return profiles, but the upper and lower performance constraints are substantially similar in most if not all cases.

This document or presentation is intended for institutional investors and/or wealth advisers only, and is not intended for distribution to others. Halo Investing, Inc. (“HII”) is a parent company of Halo Securities, LLC (“Halo Securities”). HII is not a registered broker-dealer or registered investment adviser. Securities are offered through Halo Securities, which is an SEC-registered broker-dealer and member of the Financial Industry Regulatory Authority (“FINRA”) and the Security Investor Protection Corporation (“SIPC”). Halo Securities is affiliated with Halo Investing Insurance Services, LLC. Halo Securities acts as distributor and selling agent for certain securities offerings and is not the issuer or guarantor of any security. For more information about Halo Securities, you can visit https://brokercheck.finra.org/firm/summary/279029. For more information about Halo Investing Insurance Services, LLC, you can visit https://secure.utah.gov/agent-search/organization Details.html? agent=ZPQy806YK4. For more information about the content of this document, contact marketplace.sales@haloinvesting.com.