What’s Ahead:

- Layering structured notes into a portfolio of mutual funds and ETFs creates an allocation with reduced risk while offering enhanced upside return potential.

- Cash is attractive right now in the eyes of retail investors, but its near-term benefits might come at the expense of not hitting long-run goals.

- Growth and income notes offer some of the same certainty through their defined-outcome nature and can keep individual investors on a path to achieving their objectives.

I hate losing. I hate losing even more than I want to win. There’s a difference.”

– Billy Beane, Moneyball

That’s a line from the famous baseball movie Moneyball during a scene in which Oakland A’s general manager Billy Beane (played by Brad Pitt) was instilling in his players the virtues of working hard, fighting against the odds, and fulfilling the team’s mission.

The same contempt for loss is apparent when it comes to investing. Losing feels awful. Seeing your net worth drop during bear markets after slow and steady climbs during bull markets makes it all feel for naught.

Bad Behavior

It’s called “loss aversion”—a behavioral quirk that makes our brains feel the impact from losses about two-and-a-half times more than we enjoy the pleasure of a gain. While that cautious mental disposition aided us as we fought for survival on the Serengeti Plain eons ago, it works against us in modern financial markets. Playing it too safe at the wrong time can lead to poor outcomes when it comes to reaching near- and long-term goals.

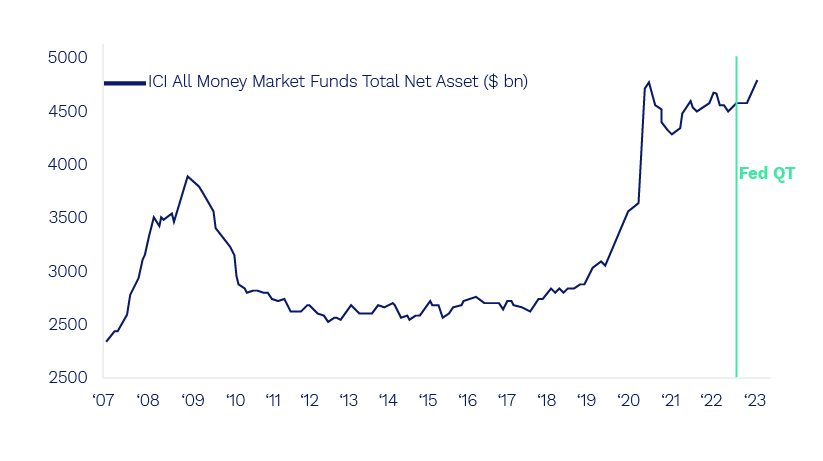

Investors Piling Into Cash

How does that apply today? Consider that the start of 2023 featured massive inflows into money market mutual funds. According to fund flow data from EPFR, investors piled more than $135 billion into global money markets in just a few weeks—that’s the highest sum since the height of fear during the pandemic. What’s different now, however, is that volatility, while still elevated, is nothing like what was seen in the first two quarters of 2020. It’s not so much a fear of big stock market losses today, but the appeal of a reasonable yield alternative.

Money Market Madness

Cash Levels at All-Time Highs

U.S. money market funds saw net assets hit all-time high

What’s not to like? With a few clicks, you can earn more than 4% by stashing cash in an account with virtually no risk and avoid ongoing volatility in the stock market as well as uncertainty about how the bond market will perform after its worst year on record.

Cash Is Safe Now, but Risky Long Term

The problem is that hiding out in cash feels so good—like a warm blanket next to a fire. It can burn you, though. Investors are unlikely to hit their long-run objectives even with a relatively high and safe money market yield. To put it bluntly, more risk must be taken to earn a higher return. Now, you might think that more risk means allocating to stocks with a buy-and-hold approach and just accepting the volatility that comes with a low-cost index fund. Sure, that is a choice, but there’s a better way to go about asset allocation that can offer downside protection with the potential for enhanced upside participation.

Concerned About Volatility? Consider a New Portfolio Solution

Going overweight cash via a high-yield money market fund is a fine tactical play right now. A little extra dry powder fits into a target asset allocationthat includes active and passive funds and structured notes. In Halo’s view, an asset allocation strategy using structured notes layered into a portfolio of equity and fixed-income funds is an easy and effective way to hedge against volatility without missing out on the market’s upside.

How to Layer Structured Notes As an Equity Hedge

Here’s how it works: For each sub-asset class, such as U.S. large-cap growth, the investor holds, say, a 2% position in a 3- to 5-year growth structured note with an underlying asset matching that sub-asset class (the Russell 1000 Growth Index in this hypothetical case). Alongside the note might be a 5% weight in a separately managed account (SMA), active mutual fund, and/or ETF. Similar breakouts among asset classes and styles are constructed throughout the portfolio.

There are customization options with this portfolio method, too. It is important to recognize that a longer-term note can be used if more upside potential is desired. For less volatile sub-asset classes, such as U.S. large-cap core and U.S. large-cap value, 30% of total exposure to that niche can be allocated toward a growth structured note. For higher volatility sub-asset classes, like U.S. small-cap core and emerging markets, consider staking 50% of exposure to a growth structured note.

Liquidity and Portfolio Management Capabilities

That is the general allocation construct. Now here is where we can get more tactical with portfolio management. The long equity sleeve through the funds (an active mutual fund or ETF) can be used as a “cash toggle” in a few ways:

- Active bets: With the liquidity of the funds, an advisor can move in and out or adjust the size of the position based on an equity market thesis. The growth notes act as a ballast to the portfolio and can be thought of as a core or anchor in case the tactical idea underperforms—the client will be glad they had the notes.

- Short-term cash solution: If there is a liquidity need, the advisor does not have to sell the structured notes. Rather, simply draw cash from the funds or dry powder from the money-market allocation.

- Tax-loss harvesting: Through the layered approach, the funds can be used to generate losses easily while still holding notes in the portfolio. So, the same benefits of traditional portfolio management are achievable.

Shrinking the Behavior Gap

A hedged equity strategy with layered notes helps to protect against market declines as well as mitigate the risk of active funds underperforming their benchmark during bull markets. In addition, the so-called behavior gap is narrowed since clients can be confident about staying invested during uncertain times. Getting back to the current situation of enticing short-term yields, a portfolio of structured notes takes advantage of better rates today, since they have a fixed-income component, while having the ability to get clients to their goals.

How to Put Income Notes to Work

Maybe you have clients that are simply too nervous about taking significant market exposure despite the appeal of downside protection and enhanced upside through equity-linked growth notes. There’s a solution for that common situation: income notes.

Income structured notes can be put to work in the equity sleeve of the portfolio to generate strong yields with defined outcomes. Put simply, income notes are generally less volatile than growth notes, and they can lock in yields to meet a risk-averse client’s return objectives.

The Bottom Line

A year or two ago, who would have thought you as an advisor would be fielding questions about where to earn a 4%-plus safe yield on short-term savings? That’s how quickly things can change in the investing environment. To keep investors focused on hitting their goals, a broader portfolio allocation is needed that can reduce downside risk while offering upside returns over the long run. Growth and income structured notes layered into a traditional asset allocation can be a solution to keep investors on track.

Please see our Halo Disclaimer for other important disclosures.