Key Takeaways:

- Rising stock-bond correlations challenge traditional diversification and long-standing 60/40 assumptions

- Clients would like growth, income, and protection — without the usual tradeoffs

- Structured Note SMAs are designed to provide a flexible, outcome-driven approach to modern portfolio construction

The great bond bear market of 2022 is further in the rearview mirror. Investors are focused on new challenges at hand, both domestic and international. But that post-pandemic year may have marked a turning point in asset-class correlations.

Coming into 2022, bonds provided reliable diversification to stocks. Treasuries zigged when equities zagged, and investors near or in retirement could lean on the traditional 60/40 allocation for solid returns with muted volatility.

From four years ago to today, the market landscape has changed. Interest rates have become one of those risk factors that routinely send stocks lower, and intermarket dynamics may be in a new secular regime. Inflation, bond market volatility, and geopolitics have all ramped up. It’s a global story, too — rising sovereign interest rates around the world offer little help when seeking diversification.

New solutions are needed. Creative, yet disciplined, strategies must be crafted and honed to help individual investors weather the new financial climate and reach their goals. For financial advisors, a different approach appeals to today’s savvier clientele. Professionally managed Growth and Income Structured Note separately managed accounts (SMAs) can drive new business, cultivate current relationships, and improve advisory workflows.

Clients Want Outcomes, Not Allocations

Today’s investors are less concerned with how their portfolios are constructed and more focused on what those portfolios can deliver. Broadly speaking, they want growth, but not at the cost of a significant drawdown. They want income, but without taking on undue market risk. And they want to participate when equities rally without feeling overexposed to volatility.

Their demands are high, and they are not shy about seeking the advisory firm that will address their wants, needs, and desires. Wealth managers winning new business are those who provide solutions that balance growth, protection, and income.

Rethinking Portfolio Construction

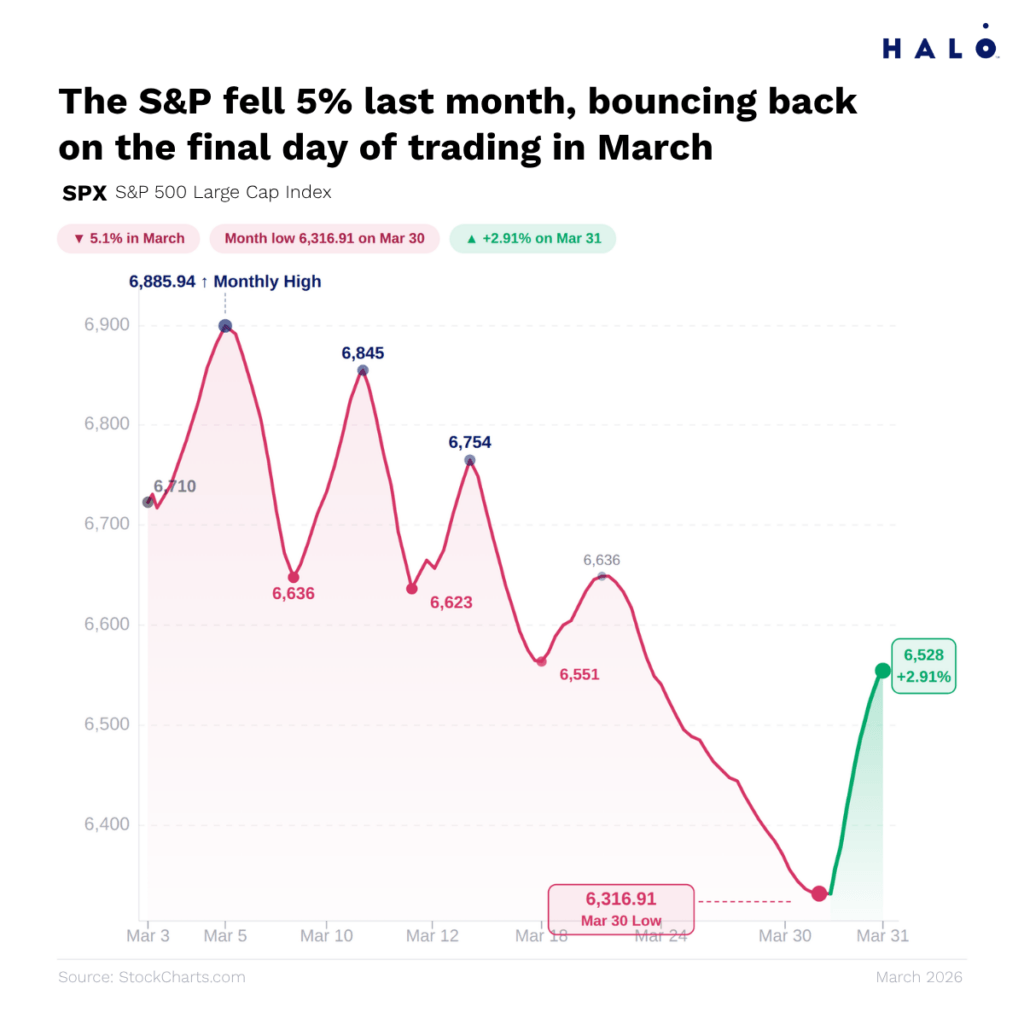

To address these challenges and meet your clients — both current and prospective — where they are, advisors must explore avenues beyond static allocations. The conventional 60/40 portfolio performed well from April 2025 through this past February. A risk-conscious investor, maybe a retiree, likely felt upbeat about their net worth. Then March came in like a lion.

The war in Iran sent oil prices soaring, stocks plunging, and interest rates higher. Even gold and silver cratered. It was like 2022 all over again — a year when the 60/40 declined by more than 16%, not including inflation. It served as a reminder that risk happens fast, and a portfolio that might look diversified on paper can quickly fail to cushion the blow when correlations go to 1.

The goal is not to replace traditional investments entirely, but to complement them with strategies designed to deliver equity-like returns, incorporate downside protection, and potentially generate high income — all within a more intentional framework. Structured Notes may be one vehicle to produce returns that may help address inflation risk, generate uncorrelated income, and deliver performance with a lower beta to the global economy.

The Importance of Timing and Flexibility

To be clear, passive investing has its advantages. Ultra-low-cost products and direct exposure to specific asset classes, markets, and sectors work for some clients. But not everyone is the same. One of the limitations of many traditional and packaged solutions is their rigid implementation.

When market dislocations occur, active managers in the Structured Note market can lock in favorable terms — including enhanced downside protection levels, higher participation rates, and compelling yields. Expert portfolio managers have their fingers on the pulse of what’s available when volatility spikes. It’s not market timing; rather, it’s flexibility and acumen.

Why Mid-Cycle Investing Can Be Problematic

We may be in the Jan Brady part of the economic cycle — the unsettling middle space between optimism as a new growth regime sets in and the boom characteristics toward the end of an economic expansion. It’s at this stage that timing risk is especially relevant.

Investors entering mid-cycle may not receive the same level of downside protection or upside potential as those who invested at the start. The result is a mismatch between expectations and reality. A more dynamic approach can mitigate this issue by continuously assessing opportunities and building portfolios with staggered exposures and varied maturities, reducing reliance on any single entry point. That’s where Structured Note SMAs demonstrate their value.

Bridging the Income Gap

We’ve focused on portfolio construction, the importance of manager flexibility, and the cyclical risks facing investors. But let’s be direct — many clients simply want a defined outcome with a high yield. That’s hard to come by in today’s correlated stock and bond markets, which can be upended by a single social media post or a disappointing economic report.

Asset classes are moving together, and inflation persists. Delivering steady, real yields is not easy. Strategies that integrate income generation with growth and risk management can be a needle-mover with clients. Structured Note SMAs with contingent income and defined protection levels may help address the dual need for cash flow and capital preservation.

Liquidity, Hidden Costs, and Transparency

Structured Note SMA investing is not a portfolio elixir, nor a shortcut to retirement — but some features are more beneficial than advisors might expect.

Liquidity is often cited as a core advantage of ETFs, which offer intraday trading throughout the trading day. Structured Note SMAs operate differently — liquidity is available, but Structured Notes are typically bought and sold in the secondary market, which means pricing and execution can vary based on market conditions, dealer availability, and the specific terms of each note. Investors should understand that exiting a position before maturity may result in receiving less than the original principal, particularly in adverse market environments. For clients with shorter time horizons or unpredictable cash needs, this is an important consideration.

That said, daily tradability is not without its own costs. Maintaining intraday liquidity in complex structures can introduce inefficiencies and performance drag. For clients with longer time horizons who prioritize defined outcomes over flexibility, the liquidity tradeoff of a Structured Note SMA may be a reasonable one — provided it is clearly understood upfront.

Transparency is another dimension worth examining carefully. Advisors and clients have historically been cautious about investments they cannot fully see or understand. The NewEdge Investment Solutions SMA is designed to provide visibility into the underlying Structured Note holdings within the portfolio. Advisors should confirm directly with NewEdge the specific level of holding-level disclosure available to clients, as transparency features can vary by manager and platform. Greater visibility into the portfolio’s components can help advisors communicate more clearly about the role each position plays — but advisors should conduct their own due diligence on reporting capabilities before recommending this strategy.

What Advisors Should Know: Potential Risks of Structured Note SMAs

Structured Note SMAs are not without meaningful tradeoffs, and a balanced view requires understanding the risks alongside the potential benefits.

Issuer credit risk is one of the most important. Structured Notes are unsecured debt obligations of the issuing financial institution. If the issuer were to default, investors could lose some or all of their principal, regardless of how the underlying index or asset performed.

Liquidity constraints are also a practical reality. Unlike ETFs or mutual funds, Structured Notes do not trade on an exchange. Secondary market transactions depend on dealer availability and prevailing market conditions. Investors who may need access to capital before a note’s maturity date should weigh this carefully.

Capped upside is a third consideration. Many Structured Notes that incorporate downside protection do so in exchange for a cap on maximum returns. Advisors should ensure clients understand this tradeoff — defined protection has real value, but it is not free.

These risks do not disqualify Structured Note SMAs from a portfolio role by any means, but they do underscore the importance of suitability assessment, clear client communication, and ongoing portfolio review.

The Bottom Line

The pressure on traditional model portfolios is unlikely to ease. Stubbornly high correlations, uncertain return expectations, and evolving client demands all point toward the need for change. This does not mean abandoning diversification or long-term investing principles. Instead, it suggests that these principles may need to be applied in more flexible and adaptive ways.

For advisors, today’s environment presents both a challenge and an opportunity. Structured Note SMAs — and the outcome-driven framework they support — may be worth exploring as one component of a broader client service approach, particularly for those clients whose goals and risk tolerance align with the characteristics of this structure.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and informational purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and is not intended to portray a recommendation to buy or sell a particular product or service.