What’s Ahead:

- Alternative investments are springing up left and right. Advisors might be left unsure which could be good fits for client portfolios.

- Halo’s protective investment solutions don’t require learning about esoteric assets or paying opaque fees.

- Our defined-outcome products and platform are designed with the needs and desires of the registered investment advisor (RIA) in mind.

Alternative investments are in the news once again. Steep losses in both the global stock and fixed-income markets have left investors in search of protection. Earlier this month, it was reported that two brokerage behemoths, Blackrock and Fidelity, were moving toward creating more alternative investment funds. Ongoing volatility in equities and unprecedented losses in bonds this year are reshaping the industry. RIAs now have more options than ever when it comes to constructing and managing client portfolios to buffer against real-return losses for the typical 60/40 allocation.

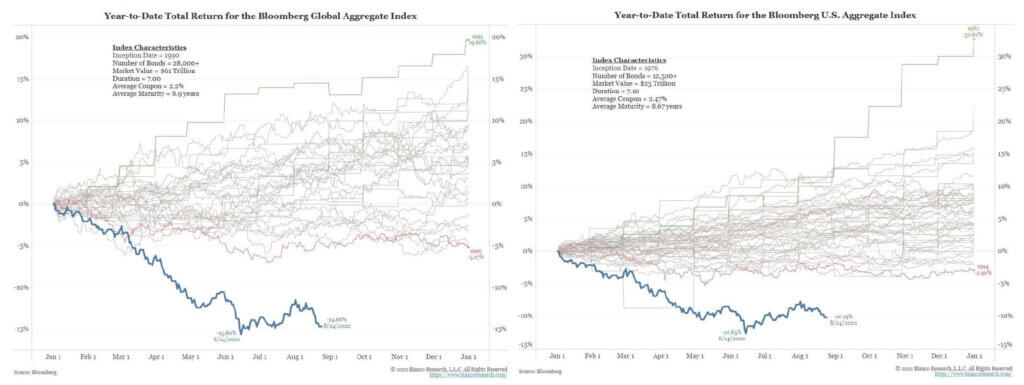

Fixed Income Losses Mount As Higher Rates Persists: 2022 On Pace As The Worst Year On Record

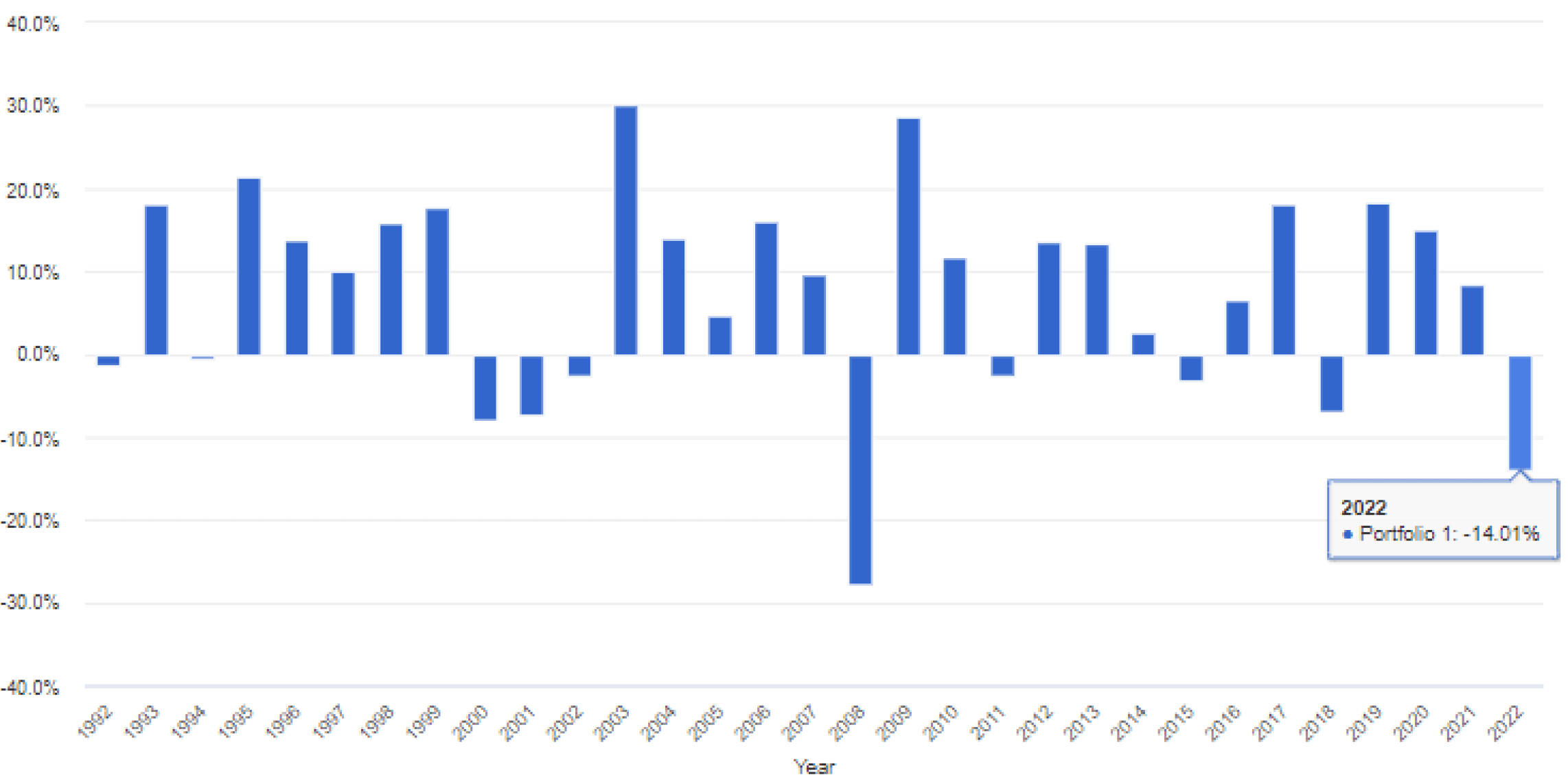

Global 60/40 Portfolio: Inflation-Adjusted Returns By Year (2002’s Performance Through July)

The Paradox Of Choice

So many choices often create confusion, however. A surge in various types of so-called alternatives – from crowdfunded real estate to art, wine, farmland (and so many more) – makes an advisor’s job all the more difficult. An explosion of “alts” leaves wealth managers increasingly having to explain periodic valuation changes in niche assets, not to mention their contribution to a portfolio’s overall results. In reality, most RIAs are busy enough managing client assets, operating a business, learning about new tax laws, and cultivating relationships to learn about an ever-growing list of assets seeing large inflows.

No Need To Become An Expert

Halo Investing’s protective investment solutions do not require upskilling to learn about new products and a hot ‘alternative-of-the-day’. Imagine the uncomfortable client meeting after a lousy quarterly performance report from an alternative investment – you must be able to explain why that asset or fund did poorly.

By teaming with Halo, all you need to understand is something you probably already know: how the stock and bond markets work. Structured notes, for example, are priced off an underlying index (such as the S&P 500) with a specific downside protection amount and defined upside participation. Those terms are outlined and described with clarity on the note’s fact sheet. So there is no esoteric micro-asset class to research. If you do have questions, Halo’s team of subject-matter experts is on hand to walk you through how notes work and instill confidence through the transaction process.

Transparent Fees Are A Must

Another problem with alternatives popping up in today’s investment landscape is their fee structures. Many emerging “alts” can be just another way for investment managers to collect high fees in a world of compressing brokerage margins and collapsing index fund expense ratios. RIAs are cautioned to fully understand what they are paying for with alternative investments as well as any additional fees that may be charged simply to hold an account.

Keeping A Long-Term Perspective

A third issue both risk-conscious investors and those with an aggressive long-term horizon must weigh now is what happens if markets manage to recover. The last thing an advisor wants to do is park client cash in assets that go on to underperform. At Halo, we’ve discussed the Equity Repair Strategy in recent weeks considering the significant drop in stocks. With our protective investments, including buffered ETFs and structured notes that offer upside market participation, client portfolios can be positioned to take part in a market recovery.

The Advisor Is Front And Center

Halo Investing is unique in that we keep the advisor top of mind. Structured notes, annuities, and defined-outcome ETFs offered through our platform are designed to help RIAs grow their business by taking control of portfolios and defining risk for clients. Alternative investments offered through various other firms are meant to simply provide yet another uncorrelated asset to own, which can be a headache in terms of learning about the product, and the firm offering it, as well as the ongoing account maintenance. Moreover, Halo’s protective investments are meant for long-term financial planning and risk management, not just as assets to round out a portfolio.

The Bottom Line

Advisors can stand out in the market using Halo Investing’s tech-driven platform. Our marketplace offers a straightforward structure to add risk-defined notes, annuities, and buffered ETFs to client portfolios. While today’s zoo of possible alternative investments might look enticing, there are several problems with adding so much complexity. Our ecosystem and technology bring costs down and empower advisors to seamlessly build and manage portfolios of products that have defined-investment outcomes.

Please see our Halo Disclaimer for other important disclosures.