What’s Ahead

- Markets react to trends faster than ever, resulting in periods of quickly rising volatility in both the stock and bond markets.

- A new index seeks to take advantage of shifting macro factors.

- The traditional 60/40 portfolio proved its possible peril in recent years, and advisors should demand better alternatives.

Get ready for a new market paradigm. As technology has progressed, along with increasing demand for customized portfolio solutions for a range of client outcomes, dynamic asset allocation has grown in prominence. In response, a new index seeks to quickly adjust to markets that now seem to move faster than ever.

The S&P Market Agility 10 Index (the “Index) uses the S&P 500 and Treasuries to harness volatility while capturing gains across stock and bond markets. As the name suggests, the Index targets a 10% volatility figure over time. Think of volatility like the CBOE VIX Index – the S&P 500’s average volatility over time has been roughly 20%, so the S&P Market Agility 10 Index seeks half the volatility of U.S. large caps.

It does this by dynamically allocating into and out of the S&P 500 and Treasuries based on quantitative factors like momentum, volatility itself, changes in the yield curve, and other interest-rate spreads. It might sound technical, but this adaptive approach has been around a while for advisors. There are existing funds that seek to actively re-allocate to stocks, bonds, commodities, and cash, but innovations now allow for an expanded suite of portfolio tools for today’s retail wealth managers. Structured notes and insurance products are such examples.

Understanding the S&P Market Agility 10 Index

Here’s how it can work: For the stock slice of the Index, a long or short position can be taken to mimic exposure to the S&P 500. During periods of positive momentum, the Index may be long. When a correction occurs – and volatility rises – the Index can switch to a short stake. In another situation, a rapid interest rate increase driven by inflation may warrant a short equity position.

So, the Index is a partial play on the momentum factor – one of the longest-standing and historically significant factors for the U.S. stock market. The Index uses quantitative inputs to adjust allocation weights to stocks and bonds daily based on real-time, intraday market conditions.

Let’s talk about the fixed income piece. Investors are probably familiar with the perils of maintaining a static allocation to bonds. Since they are sensitive to changes in interest rates, macro factors can have a loud say in short- and intermediate-term returns. Modern markets now seem to ebb and flow based on gyrations in the rates markets; correlations between stocks and bonds are no longer outright inverse – they are commonly positively related. Thus, it’s possible that the Index may have long exposure to both the S&P 500 and the Treasury market. Alternatively, the Index may be short both stocks and bonds, perhaps during a period of heightened inflation risk.

Understanding the S&P Market Agility 10 Index

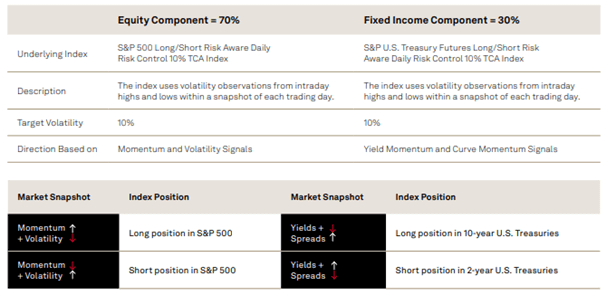

The S&P Market Agility 10 Index’s Neutral Position and Adjustments

The neutral position is a 70% long stake in equity exposure and a 30% long stake in Treasury exposure. It then applies an additional risk-control mechanism that targets the 10% volatility level mentioned above. From there, the Index dynamically adjusts the allocation based on price signals, momentum, and volatility shifts.

Now, here’s the exciting part from a portfolio management perspective: Both components (equity and fixed income) use intraday volatility observations. Rising momentum and declining volatility generally result in higher equity exposure, while falling momentum and rising volatility trigger a fast net shift away from long-S&P 500 exposure. For fixed income, falling interest rates and a steepening of the 2-year/10-year Treasury yield spread result in the Index taking on more duration exposure (this can include going short the 2-year Treasury note).

Separating the S&P Market Agility 10 Index from other indexes or products is its dynamic two-step, reallocation method and quickly changing approach. Today’s faster market cycles, including shorter-lived corrections, should require a more nimble risk-control tool.

How the Index Works

“Interesting Stuff, Why Should I Care?”

Too many investors were caught flat-footed when interest rates began to rise in 2020. A steep bond bear market was devastating for some retirees who depended on steady returns from the traditional 60/40, stock/bond portfolio. The S&P Market Agility 10 Index and products based on it are designed to be better diversification tools.

Its multi-asset construction and ability to take on long or short stock and bond exposure make it a potentially compelling vehicle for today’s retirees who rely on a portfolio to meet daily living expenses, or even just folks who have a near-term financial goal.

Why Now?

Along with today’s fast-moving markets, geopolitical jitters and uncertain fiscal and monetary policy seem to result in sudden bouts of volatility. The S&P Market Agility 10 Index shows impressive long-term gains when applying its methodology to actual market conditions over the past several cycles, including the latest period of macro risks.

As of late 2024, its 10-year annualized return would have been just shy of 11%. It’s true that the compounded annual growth rate falls shy of the S&P 500’s, but performance has come with much lower volatility versus a 100% long equity position. Now may be the ideal time to offer investors access to vehicles that can weather a market environment marked by higher volatility and lower returns compared to the regime of the past decade-plus.

The Bottom Line

Dynamic asset allocation could be the next big shift in the portfolio management world. Advisors seeking to offer better risk-controlled investment products should take a hard look at products tied to the S&P Market Agility 10 Index. The 60/40 allocation can work in some scenarios, but we’ve seen how poorly it can serve risk-conscious investors when macro factors turn a certain way. New approaches are required to help retail clients attain their financial goals and meet today’s fast-changing markets.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and information purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and are not intended to portray a recommendation to buy or sell a particular product or service.

US307/1.0/2501