What’s Ahead:

- A new survey underscores the value of serving a specific client type, so an advisor’s productivity is maximized.

- While annuities and Structured Notes are commonly thought to be relegated to retirees, other types of investors can benefit too.

- Defined-outcome investments can be tailored to any individual’s risk and return goals.

One of the major trends in the advisory industry over the past decade-plus is the niche concept. The notion of focusing on a seemingly small subset of the investment populous—so an RIA’s services are unique and specific to one type of client—is thought to deliver more value. Casting a wide net to bring in clients from every walk of life and in every financial stage of life is often too broad and hampers the advisor’s ability to deliver quality services.

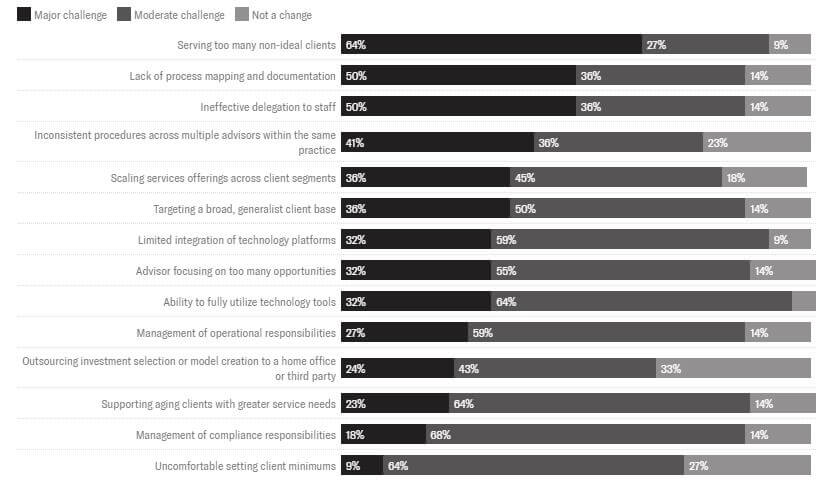

A new study from Cerulli Associates underscores the benefits of scaling down. According to the April 2023 Cerulli Edge – U.S. Advisor Edition poll, the top productivity challenge among wealth managers today is serving too many non ideal clients. A high 64% of advisors report it as the biggest problem with just 9% saying it’s not an issue.

Productivity Hack: Niche Down

Selecting one group of investors, type of professional, age range, or even a certain hobbyist category could lead to a more streamlined business and more fulfillment. Advisors commonly find that the goals, fears, and financial priorities of individuals and families within each niche tend to be consistent. So, once you, as the advisor, encounter a complex planning task, you’ll eventually come across it again and be able to deliver premier services with confidence.

For wealth managers working with clients nearing or in retirement, protecting a portfolio is usually near the top of the list of financial priorities. And that spans the niche spectrum—whether you work with retired airline pilots in Atlanta or cater to former classroom teachers in New England, protecting assets from inflation, taxes, and market losses is a universal goal these days. Protective investment strategies can help most advisors who have niched down with their service offering no matter the age range of investors, though. Let’s explore how annuities, structured notes, and buffered ETFs can effectively be used to improve financial plans across client types.

Annuities

Individuals and couples approaching and in retirement are often the most likely to be interested in annuities. Having more guaranteed income to ensure daily living expenses are met and that longevity risk is minimized are key goals. Immediate income annuities can secure a predictable income stream, just like how a pension provides security to a retiree all while guaranteeing income for a lifetime. A survivor rider can be used to protect the risk of the contract owner’s spouse living longer, too.

But even for advisors working with people in their accumulation years, annuities can be a useful option. Consider a couple in their 40s with a significant asset base seeking to bolster their retirement plan. By contributing to an annuity during their high-income years, they can take advantage of tax-deferred growth, and then have a larger payout once they call it quits from full-time work. Both fixed and variable annuities can be used to build wealth over years and decades, and the latter type offers tax-deferred growth potential similar to funding an IRA but without strict income and contribution limits. An advisor serving a specific clientele can become an expert in a select set of annuities to solve financial challenges and instill confidence in her clients.

Structured Notes

Like how annuities can fit into a financial plan, structured notes are protective investment vehicles that can be thought of as a hybrid between stocks and bonds. Notes are commonly segmented as an alternative asset type, too. We like to think of them as “an alternative to alternatives” in the sense that notes do not come with extreme fees and zero liquidity, like so many sub-optimal alternatives that have sprung up over the past several years. Technology and competition have brought down the costs of transacting and owning structured products, too.

Another benefit is that an advisor does not have to learn about a new investing sub-asset class—structured notes are straightforward in that they are based on returns of stocks and bonds—something advisors know well. That makes explaining the return outcomes to clients easier and less stressful. Sitting down with a risk-conscious couple to outline how a note can deliver a high yield with minimal risk is usually received with optimism rather than confusion by the clients. Income notes are popular with older investors. But if you work with a niche that is of higher risk tolerance, then you can include growth notes that work similarly to equities but with enhanced upside market participation.

Buffered ETFs

Another universal investment solution that is gaining ground in terms of asset flows is buffered funds. These ETFs work similarly to a structured note but in the ETF wrapper. Their daily NAV and share price will vary like any stock or fund, but the ultimate return is based on a maturity date, underlying asset or index, protection amount, and payoff construct. Also known as defined-outcome ETFs, the strategy employs options contracts to set a predefined range by which the ETF offers protection from market declines. Downside risk control is set using options.

For instance, a 10% buffer means that a principal investment is protected against the first 10% drop in the reference asset or index. But if you work with a client niche that is generally more tolerant of risk, then you can include higher-growth potential. Halo’s buffered ETF platform displays each fund’s return at maturity percentage and expected annualized return, which helps advisors create the right strategies. Finally, reference assets include the S&P 500, Russell 2000, international indexes, and long-term Treasury bonds.

The Bottom Line

Advisors are more pressed for time than ever. In a world of constantly changing regulations and technology disruptions that can be intimidating to grasp, focusing efforts on solving client challenges may seem daunting, but targeting a certain investor type could be the right strategy to streamline your practice. Finding individuals and families facing similar financial hurdles and with like-minded goals makes tailoring an investment plan easier and with better scale. Protective investment strategies can be employed in diverse ways depending on your niche.

Annuities are not suitable for all investors. All recommendations for annuity products must be suitable and appropriate for the client and must be based on a thorough fact finding and understanding of the client’s unique financial situation, needs, goals, and risk tolerance.

Please see our Halo Disclosure Page for important disclosures.