Key Takeaways:

- Principal Protected Structured Notes blend downside protection with market-linked upside participation

- Today’s higher interest rates may enhance potential returns compared to past cycles

- Tradeoffs matter: maturities, caps, participation rates, and liquidity, alongside client goals, must be considered

Markets don’t move in straight lines. Even during a bull run, periodic setbacks — pauses, pullbacks, corrections, and sudden plunges — keep investors on edge. For clients approaching key financial milestones, volatility and sequence-of-returns risk carry both financial and psychological costs..

That’s exactly why financial advisors are increasingly turning to Principal Protected Notes, a category of structured notes designed to return the original investment at maturity while still offering meaningful participation in market upside.

This guide covers everything advisors and investors need to know about principal protected notes: how they work mechanically, how today’s rate environment affects their terms, who they may be best suited for, and what tradeoffs to communicate with clients.

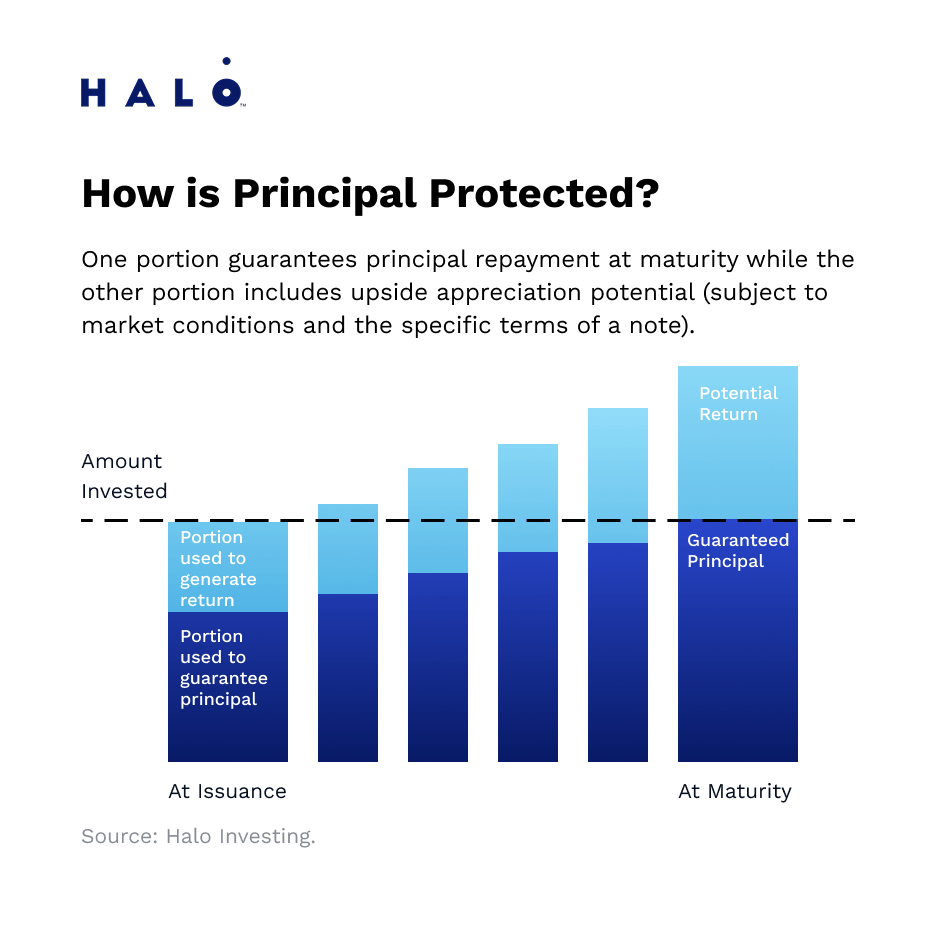

What Is Principal Protection? The Core Concept Explained

Before we dig into specific Note components, let’s lay out what “principal protection” means. It’s a guarantee, backed by the creditworthiness of a Structured Note issuer (such as a large global bank). The Noteholder is promised their original investment back at the end of the holding period, regardless of how the underlying asset performs.

So, what is principal protection mechanically? Banks typically combine a zero-coupon bond with a combination of options to construct a specific payoff structure. This package provides downside protection and market-linked upside exposure.

The result: The Noteholder has market exposure up to a cap, while the original investment is insulated from losses at maturity.

How Principal Protected Structured Notes Actually Work

Principal Protected Structured Notes are technically debt instruments issued by a financial institution. Here’s how it plays out behind the scenes:

- At maturity — The investor receives their original principal back from the bond, plus any gains generated by the options component.

- The bond allocation (80–95%) — Most of the invested capital goes into a zero-coupon bond priced at a discount, structured to grow back to par (face value) by the maturity date.

- The options allocation (5–20%) — The remaining capital purchases options on a market index or other underlying asset, providing the upside exposure.

Why Today’s Interest Rate Environment May Favor Principal Protected Notes

Higher interest rates can work in favor of principal protected note structures. When yields on Treasurys and corporates are elevated (as they are today compared to much of the post-2008 era), the zero-coupon bond is issued at a lower fair value. So, more cash can be used to buy options—and that’s where the upside potential comes from.

In practical terms: in a higher-rate environment, advisors may find principal protected notes with more attractive participation rates and caps than were available during the low-rate era of 2009–2021.

Principal Protection vs. Other Downside Protection Strategies

Principal protected notes occupy a distinct niche. Here’s how they compare to the most common alternatives advisors consider.

Vs. Buffer (Hard Protection) and Barrier (Soft Protection) Notes

Other Structured Note types may seem similar to Principal Protected Notes, but they are not the same. Buffer and Barrier Notes also provide downside protection, but only to a defined threshold (often 10-30%). If the underlying asset falls more than the buffer/barrier, the Noteholder is exposed to full or partial losses beyond that point. With full principal protection, the floor is the entire original investment (not just a partial cushion).

Vs. Fixed Annuities

Fixed annuities offer similar principal protection through insurance contract guarantees, but returns are typically fixed in advance. Structured Notes with principal protection may offer market-linked upside exposure. What’s more, with Principal Protected Notes, the investor is not locked into a predetermined yield. Another nuance is that annuities are commonly sought after for lifetime income and are backed by insurance company reserves rather than bank credit.

Vs. CDs and Treasurys

Traditional safe-haven assets, such as CDs and U.S. Treasurys, guarantee the return of capital but offer more modest returns. Principal Protected Structured Notes generally offer higher return potential in exchange for less certainty (they are not backed by FDIC insurance or the full faith and credit of the U.S. government). While Treasurys are virtually risk-free if held to maturity, Principal Protected Notes are subject to the financial failure of the issuing bank.

Today’s Market: Why Advisors Are Talking About Protective Investing Now

The Structured Note marketplace has grown substantially over the past decade, and Principal Protected Structured Notes have played a leading role. A few forces converge to make the conversation particularly relevant:

1. Elevated Valuations Are Driving Demand for Downside Protection

The bull market that began in 2009 has encountered challenges, but it’s clear that 15%-plus annualized gains are simply unlikely to last. A broad set of market valuation metrics (P/E, P/FCF, P/B, CAPE) indicates equity frothiness by historical norms.

Today’s risk-conscious investors want to remain invested, but they also desire to manage downside risk (which seems to come about ever faster in the current market regime). Fully exiting the market means potentially missing continued gains; staying fully invested means accepting full drawdown exposure. A principal protected structure offers a middle path.

2. Sequence-of-Returns Risk for Near-Retirees is Real

Zooming in, investors in their late 50s and early 60s are particularly susceptible to large stock market losses—the sequence-of-returns risk. A 30% drawdown in the years immediately before or after someone calls it quits from the 9-to-5 grind can seriously jeopardize a retirement. Principal protected investments are increasingly considered as a risk-management tool for investors in or near retirement.

3. Higher Rates Can Improve Principal Protected Note Terms

Higher market yields today help. Years ago, during the ZIRP era, advisors who analyzed these products may have found the terms unattractive for their clients. Participation rates and cap structures are potentially more lucrative today.

4. Advisors Seek Customization as Goals-Based Investing Proliferates

Gone are the days of cookie-cutter portfolios and static allocations. Today’s savvy investor demands unique strategies and vehicles to help them achieve their goals. Structured Notes are like the Swiss Army Knife of protective investing, and they can be used to meet a variety of objectives.

A Principal Protected Note’s maturity, underlying asset, protection level, and return/payoff can be crafted any which way. This flexibility has made them increasingly popular among fee-based advisors seeking precise portfolio construction tools rather than off-the-shelf products.

4 Key Components of Principal Protected Notes

Understanding these four components is essential for comparing notes across issuers and communicating tradeoffs clearly with clients.

- Maturity: The period over which a Structured Note is held. Maturities can range from 6 months to 20 years; most Principal Protected Note maturities are between 2 and 5 years. Also called the tenor.

- Underlying Asset: A Structured Note’s performance generally tracks the price return of an underlying asset (often an equity index).

- Cap: The maximum return the Noteholder can receive, regardless of index performance. A Principal Protected Note with a 30% cap will return no more than 30% even if the index gains 50%.

- Participation Rate: The percentage of the underlying asset gain that the investor receives. For example, a 90% participation rate on a 20% market gain would yield an 18% return. If the market declines, the participation rate does not apply to losses. Principal protection ensures the investor receives 100% of their original investment at maturity, provided the note is held to term and the issuer does not default.

How to Choose Principal Protected Notes for Your Clients

There is no single ‘best’ principal protected investment. A client’s risk and return objectives, as well as their existing portfolio, largely determine the most appropriate combination of Structured Note components. That said, here’s what advisors should look for when conducting due diligence:

- Issuer quality: Investment-grade financial institutions with strong credit ratings.

- Competitive terms: Compare participation rates, underlying assets, caps, and maturities across multiple issuers.

- Liquidity: Principal protected notes carry liquidity risk. Exiting before maturity may result in receiving less than the original investment. While notes are intended to be held until maturity, understanding secondary market dynamics is important. Halo Investing’s award-winning marketplace and Aura Portfolio Simulator provide transparent pricing across issuers and in-depth analysis.

- Fees: Unlike a mutual fund or ETF where expenses appear as a separate line item, structured note costs are typically baked into the product terms. In practice, this means fees reduce what the investor receives — resulting in a lower participation rate or cap than would otherwise be available. Advisors should always consider the all-in cost, be skeptical of opaque pricing, and utilize Halo’s auction technology to compare notes across multiple issuers to ensure clients are receiving competitive terms.

Who Are Principal Protected Notes For?

Principal Protected Notes are not a universal solution, but they may be a strong fit for:

- Near-retirees seeking market exposure without severe downside risk.

- Conservative investors with too much in cash or sub-optimal fixed income products.

- Clients with a specific goal where capital preservation is critical, such as a real estate purchase, education funding, or business sale.

- Advisors building model portfolios who want to blend growth potential with tailored downside protection across different market environments.

Important Considerations and Risks

There are natural tradeoffs with Principal Protected Structured Notes. Advisors should be transparent with clients about the following:

- Opportunity Cost: If markets rally significantly, the cap or participation rate may limit gains relative to direct index exposure.

- Inflation Risk: A Note that returns 100% of principal in nominal terms still loses purchasing power if inflation is elevated during the holding period.

- Liquidity: Exiting before maturity may result in a loss.

- Issuer Default Risk: The principal guarantee may not be honored if the issuer becomes insolvent.

- Complexity: Structured Notes often require careful explanation with a client.

Frequently Asked Questions

The issuer contractually commits to returning the original investment at maturity, regardless of market performance. It’s a legal obligation backed by the issuer’s credit (not a government guarantee). Evaluating issuer credit ratings is an essential part of due diligence.

Many Notes protect against a pre-defined percentage of losses (typically 10–30%); losses beyond that threshold fall on the investor. Principal Protected Notes protect 100% of the original investment at maturity, no matter how far markets fall. The tradeoff is usually a lower participation rate or upside cap.

It depends on the client’s goals, risk & return preferences, time horizon, and liquidity needs. In general, look for investment-grade issuers, competitive participation rates or caps, and maturities that fit a client’s objectives and constraints. Halo’s competition-based issuer marketplace makes it easy to compare Notes from multiple issuers side-by-side.

Notes are designed to be held to maturity. Secondary markets may exist, but early-exit values can be below par. That means a client who sells early may receive less than their original investment.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and informational purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and is not intended to portray a recommendation to buy or sell a particular product or service.