What’s Ahead:

- There are more retail investors than ever, as evidenced by a recent survey that found growing participation in the stock market.

- Risks are greater than ever for individuals without a financial strategy or money coach.

- Just like any quality sports franchise, long-term success hinges on meticulous planning and psychological preparedness. Annuities, structured notes, and buffered ETFs can play crucial roles in helping clients secure a victorious endgame.

A recent Gallup poll found that a rising percentage of Americans are investing in the stock market. That’s great news for advisors who want to see people grow their wealth. But it also brings about challenges and opportunities as it pertains to financial planning strategies.

It’s not as simple as periodically investing cash flow into index funds and calling it a day. Individual investors must have a game plan with a focus on risk management, near-term and long-run goals, behavioral considerations, and an idea of what the distribution stage of the financial journey will be like. In that sense, clients need a financial coach to keep them from straying from their money mission. (Bear with us on the financial sports puns to follow!)

Rising Retail Equity Participation

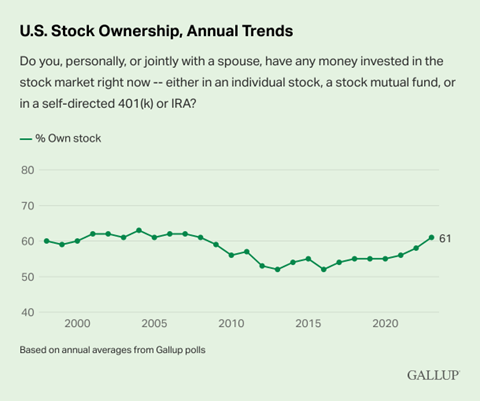

Sixty-one percent of those surveyed in the Gallup poll said either they or their spouse have money in the stock market. Most Americans invest simply through a 401(k). But with the rising use of IRAs for long-term investing, and even Health Savings Accounts, the financial account mix of most investors grows more complex year by year. What’s more, as wealth builds, new strategies are often required to better manage risk and reduce stress during market turbulence. It’s when volatility rises that people tend to make the costliest errors — driven by fearful emotions and a lack of preparation.

Preparing Today for the Uncertainty of Tomorrow

But how can advisors help people when they need it most? In what ways can a money coach provide the best pep talk and stay cool under pressure when the rest of the financial world is losing its mind? Like any good sports team, the work is done ahead of time.

The Last Dance

If you were one of the millions of folks cooped up inside your home during May and June of 2020, maybe you tuned into “The Last Dance” on ESPN. In 1997-98, Michael Jordan led the Chicago Bulls to the last of six NBA Championships along with a solid supporting cast of teammates and the “Zen Master” head coach Phil Jackson.

MJ was known, perhaps notoriously at times, for his staunch work ethic and how he would push his fellow players to be better, always focusing on the prize: hoisting that golden trophy at the end of the NBA Finals. It was through demanding work put in before and during the regular season that the team was healthy and able to finish physically, mentally, and emotionally strong.

Building a Better Team of Asset Vehicles

That’s how financial planning works, too. Halo Investing offers strategies to make individual investors’ assets work harder for them as they approach retirement and then live out their golden years. One method by which they can prepare is to diversify their investment mix away from typical stock- and bond-heavy allocations. Since most people already own equities, as evidenced by the Gallup poll, there is a growing need to build other income sources.

Annuities to Secure a Top Seed in Retirement

Have you noticed that annuities are starting to lose their negative connotation? It is something we hear about. It used to be that annuities were sold to unsophisticated individuals and couples by an “in-name-only” financial advisor. Those products were often fraught with high commissions and subpar contract terms.

Today, however, there’s more transparency with annuities, and costs are more reasonable. This was evidenced by 2022’s annuity sales boom. (It appears 2023 could shatter records, as well.) Fiduciary advisors now have the option and ease to compare annuities, tailor them to the client’s unique risks, and transact at a low cost. Diversifying through guaranteed-income strategies helps round out retail investors’ portfolios.

Don’t Lose Points During Market Volatility: Structured Notes for Bench Strength

We mentioned volatility earlier. A quality coach knows his or her players and the competition. When it comes to the advisory world, experienced wealth managers recognize that a nervous couple — one that perhaps has a very low risk tolerance — might simply freak out when the inevitable bear market strikes. This is when Structured Notes can be called on to help keep portfolios from losing a large percentage of value and to reduce psychological stress.

You see, individuals feel the pain of losses about twice as much as the pleasure from gains. This causes the herd to panic, and then liquidate positions near market lows. Structured Notes — that can feature hard protection from stock market drawdowns — are popular vehicles for managing the emotional side of the ledger and help to protect wealth built by clients over years and decades.

Higher stock and bond market volatility also works to the benefit of advisors looking to buy Structured Notes. Here’s why: When volatility goes up, the yields on Notes will be much higher to compensate the holder for a wider range of possible outcomes. Tactical advisors can manage money in a way that pounces on extreme VIX and MOVE readings by purchasing Notes to lock in higher yields. Then, when volatility eventually subsides, the Note pays a higher income stream versus traditional fixed-income products or high-dividend equities.

Buffered ETFs: The Promising Rookie Stepping Onto the Court

Finally, buffered ETFs continue to make headway among the retail investment crowd. With an increasing percentage of people participating in markets, there’s growing knowledge of what ETFs are and how they benefit long-run returns (net of fees), particularly when held in taxable brokerage accounts.

Buffered funds (also known as defined-outcome ETFs) feature a combination of market participation and downside protection, similar to a Structured Note, but in the ETF wrapper. Sure, advisors can manually purchase options and construct strategies that essentially do the same thing as today’s popular buffered ETFs, but the time and complexity of such tasks come at the detriment of growing a business. The efficiency of the ETF wrapper — from both the time and tax perspectives — makes defined-outcome funds an increasingly effective tool for busy advisors.

The Bottom Line

More Americans are participating in the stock market. That’s a fantastic trend that we hope continues. But with more people, young and old, investing in equities, there is a growing need for guidance and coaching. Additionally, as individuals and couples build wealth, the focus grows on asset protection and volatility reduction. Financial planning strategies that include annuities, structured notes, and buffered ETFs help clients — particularly those in the later financial stages of life — worry less and increase their confidence in reaching financial goals.

Annuities are not suitable for all investors. All recommendations for annuity products must be suitable and appropriate for the client and must be based on a thorough fact finding and understanding of the client’s unique financial situation, needs, goals, and risk tolerance.

An investment in structured notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Buffered ETFs’ investment strategies are different from more typical investment products, and the funds may be unsuitable for some investors. It is important that investors understand the investment strategy before making an investment. Investment involves risk, including possible loss of principal. There is no guarantee the funds will achieve their investment objectives.

Please see our Halo Disclosure Page for important disclosures.