What’s Ahead:

- Stocks and bonds declined last month as geopolitical tensions and oil prices surged, increasing equity market volatility and macro uncertainty

- Rising yields and energy-driven inflation reshaped intermarket dynamics, challenging traditional diversification approaches

- Elevated market volatility creates opportunities for Structured Note investors and defined outcome strategies amid shifting market conditions

The war in Iran has sent shockwaves across the macroeconomy, but is there hope on the horizon? To close out March, geopolitical tensions appeared to de-escalate following statements from both President Trump and the Iranian regime.

The result was the S&P 500’s best day since last May on Q1’s final session. Equities then lifted to kick off April, but worries remain about what the geopolitical landscape will look like weeks and months down the road.

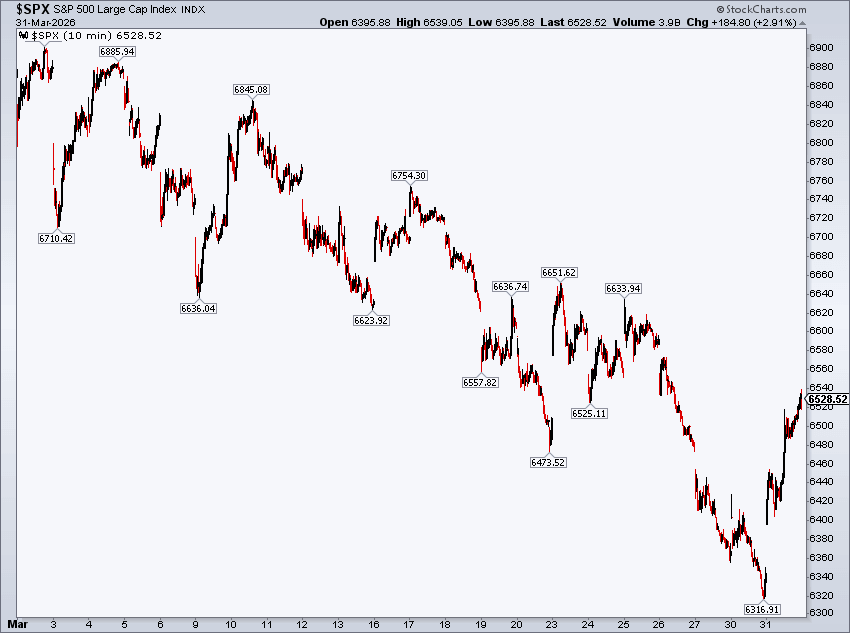

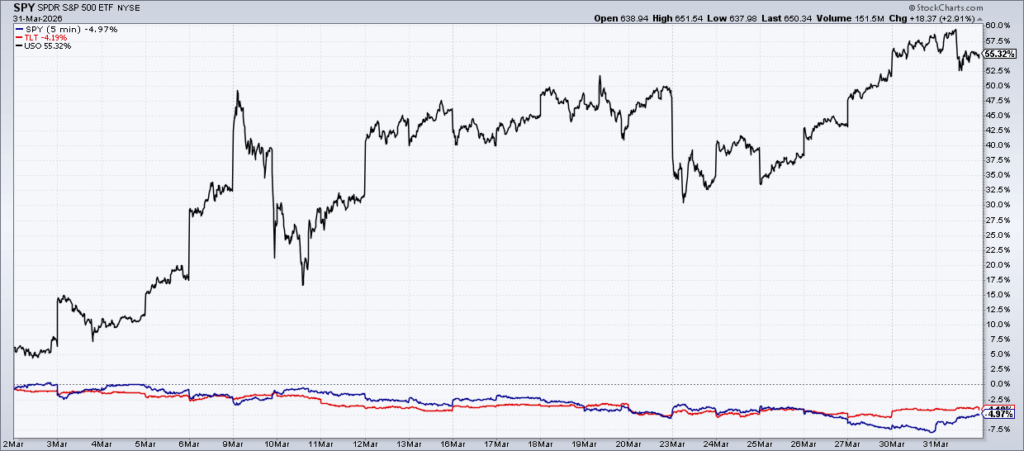

The S&P 500 Fell 5% in March, Bouncing Back on the Final Trading Day of the Month

All of it rhymes with a year ago. Recall April 2025, when global stocks fell leading into Liberation Day, then plunged immediately after the president toted out those now-infamous posterboards detailing proposed reciprocal tariff rates.

The past is never a true prologue in markets, but the first half of last year was a reminder that staying the course is often the best strategy. That period of intense volatility also underscored the new reality that diversification today looks a whole lot different than it did in past decades.

Let’s dive into what happened in markets to close out what felt like a very long first quarter. We’ll outline why protective investment strategies are more valuable than ever as investors deal with one macro shock after another.

March: In Like a Lion, and Out Like a Lion

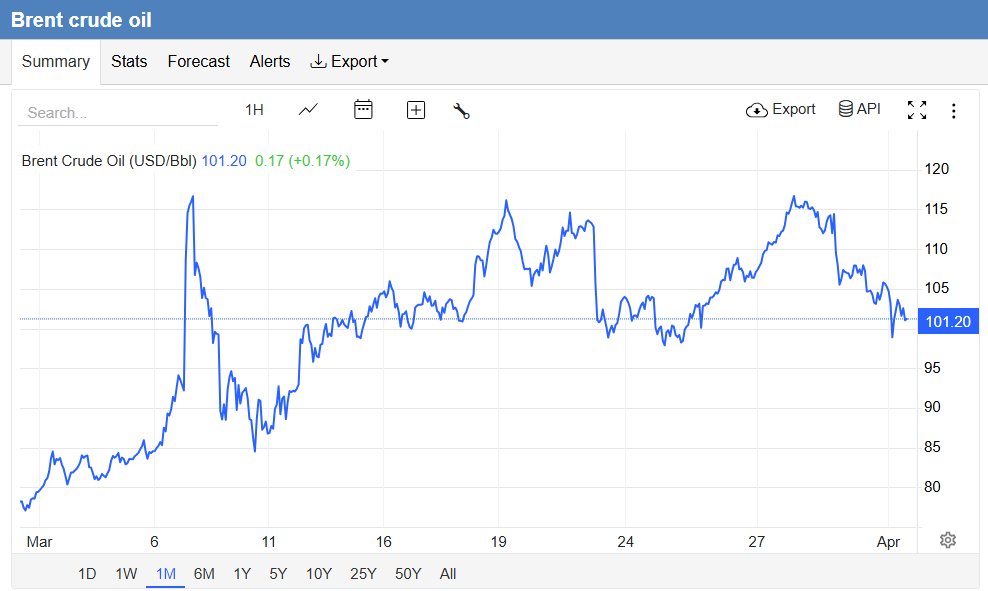

The S&P 500 fell 5.1% in March, its worst decline since March 2025. The conflict in Iran was the culprit. The key Strait of Hormuz remains effectively closed, driving global oil benchmarks to and holding near $100 per barrel. At the peak, Brent crude lifted toward $120, and some forecasters assert that $200 is not out of the question, depending on how long the Strait remains shuttered.

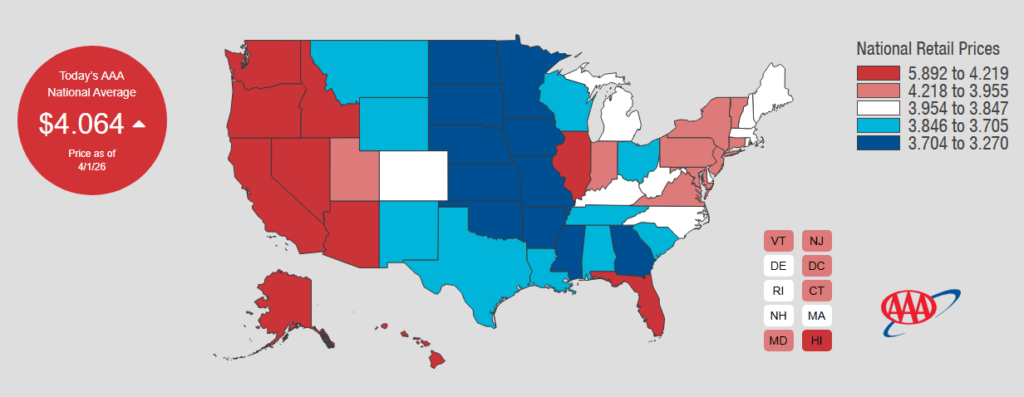

For U.S. consumers, $4 pump prices are the new reality. While retail gasoline topped $5 per gallon four years ago, the sting is still real.

Brent Crude Oil Flirted with $120 per Barrel at Times in March

AAA: Gas Prices North of $4/Gallon

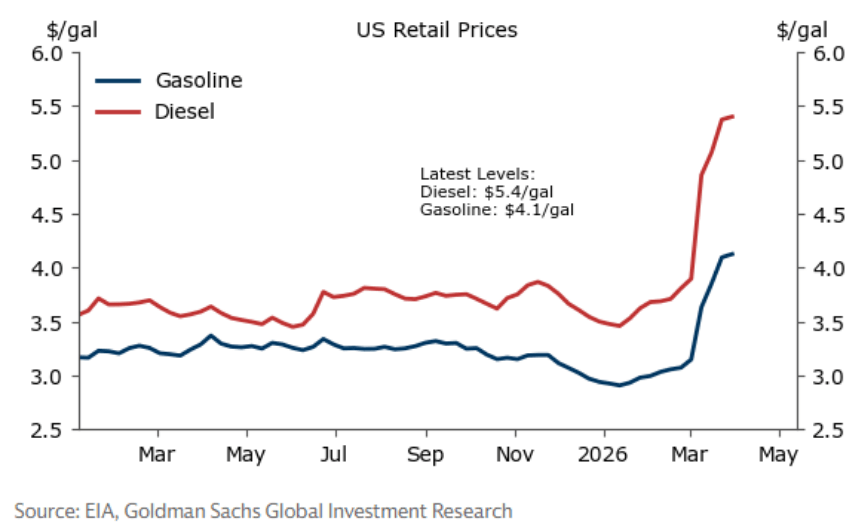

$5.40/Gallon Diesel Is a Headwind for US Businesses

Energy commodities indeed dictated price action in stocks, but they also drove changes in the bond market. The yield on the benchmark 10-year Treasury note rose from below 4% at the very onset of the war to near 4.5% by late in the month.

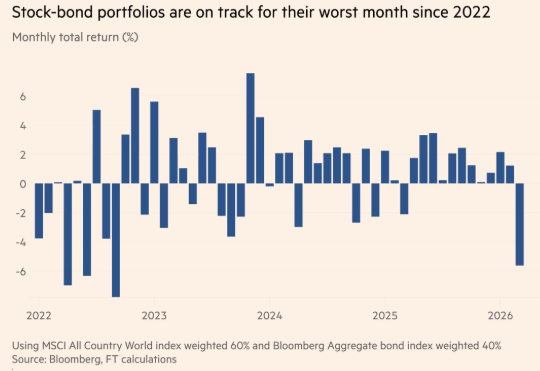

Peace talks and hopes for a U.S.-Iran-Israel resolution by the turn of the quarter eased oil prices, sending Treasury yields back under 4.3%. Throughout the month, though, stocks and bonds moved in lockstep, akin to intermarket price trends endured back during the great bond bear market of 2022.

Rethinking Diversification in an Inflationary Regime

Throughout the month, Wall Street banks put out one research note after another, adding color to the positive equity–fixed income correlation. The upshot of all that ink spilled is that inflationary regimes often link the S&P 500’s price action to the 10-year Treasury note’s price. Thus, investors are forced to seek other strategies to accomplish durable portfolio diversification.

Crude oil is thought to be one such avenue. Unfortunately, energy commodities simply don’t have strong long-term returns. So, owning, say, an oil-linked ETF often becomes a major drag on portfolio performance over the long term. Over the short run, such plays may turn into speculative bets with a wide range of potential net-worth paths.

Intermarket Themes: Stocks, Bonds Lower in March, Oil ETF Surges

Stocks & Bonds Were Down Sharply in March

Market Volatility Creates Opportunity in Structured Notes

That’s where Structured Notes and defined outcome strategies can come into play. Unlike highly volatile energy funds, advisors can craft personalized solutions that augment client allocations and narrow the range of possible financial outcomes using Notes. That’s almost always the case—what makes today different is that volatility is stubbornly high. Let’s double-click on that.

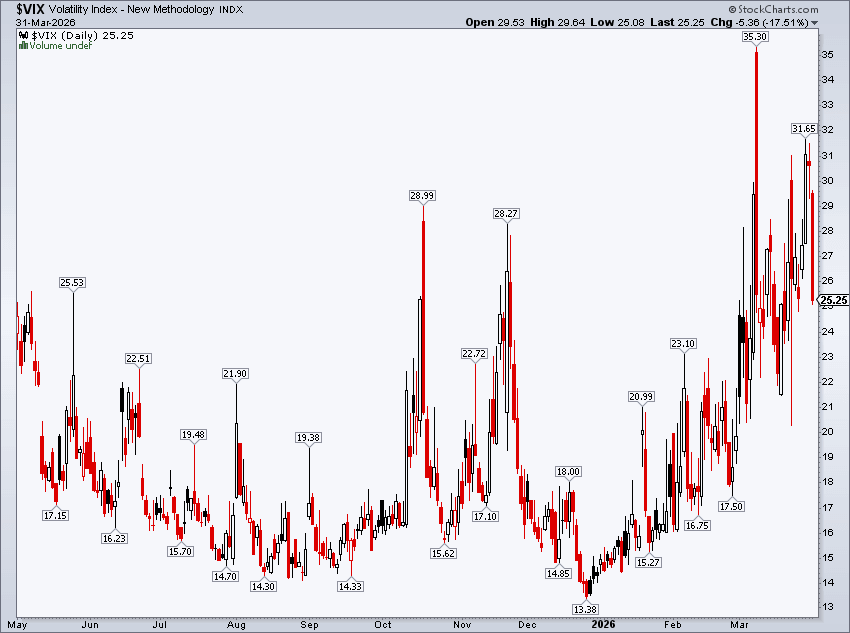

In March, the Cboe Volatility Index (VIX) rose above 30 at times. For context, that means the S&P 500 was expected to move up or down 2% day to day. The VIX’s long-term average is in the high teens, and it’s normally in the low- to mid-teens during bull markets. After dipping below 14 in late 2025, Wall Street’s fear gauge has been stair-stepping higher year-to-date as geopolitical worries have grown. That means anxiety for most investors… and opportunity for those seeking diversification in Notes.

The VIX Has Climbed Throughout 2026 Thus Far

Mathematically, higher implied volatility in the stock market means Structured Notes can potentially offer higher yields. Mechanically, when a bank underwriter creates a Note, they are essentially selling options on the underlying asset (often the S&P 500) to fund the coupon rate and downside protection level—the more they can collect, the better the terms for the Note investor. When the VIX is lofty, eyeing Growth and Income Note terms is worthwhile.

Is now the right time to put some client dollars to work in Structured Notes? We may be biased, but conditions appear favorable. As we wrote at the outset, however, it’s helpful to look back 12 months. The VIX was even higher then—near 60 for a moment—but volatility didn’t last. Those who secured Notes in April 2025 likely locked in favorable terms. The VIX plunged back below 20 within weeks.

Such a V-bottom in the S&P 500 could happen again, but nobody knows for sure. New risks are front and center, and not all of them surround the conflict in the Middle East.

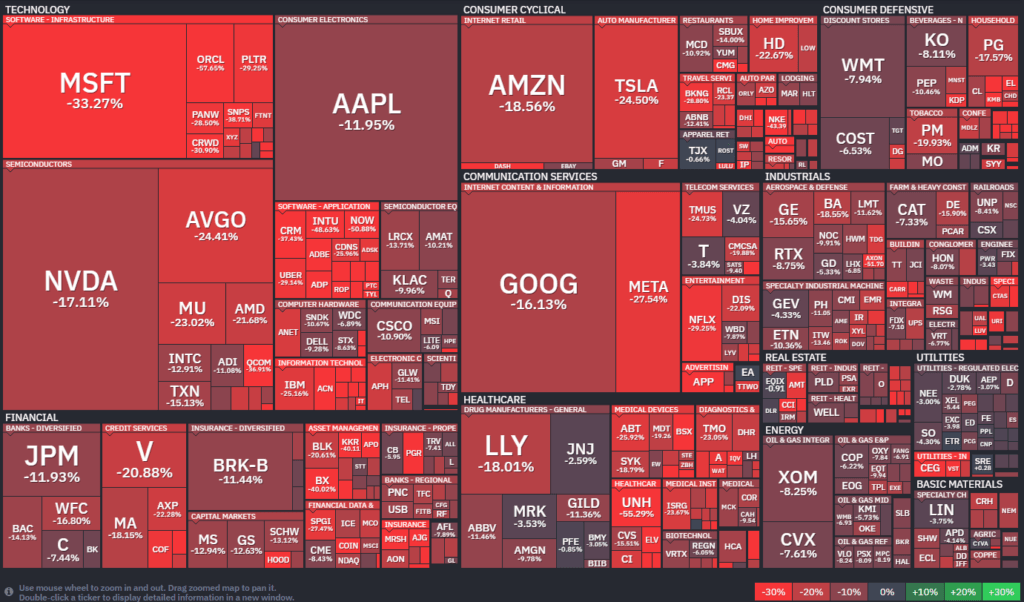

Big Tech Faces Broad-Based Market Volatility

Far removed from $100 oil, AI has brought about significant selling pressure in some areas. Last month, we spotlighted “H.A.L.O.” stocks (heavy-asset, low-obsolescence… pardon the pun) that are thought to be the most immune to AI automation and more efficient technological workflows.

That thesis is alive and well on Wall Street, and it’s really hit home for investors owning the Magnificent Seven stocks. By the close of March, every one of the Mag 7 names was down at least 12% from their respective 52-week highs. Microsoft (MSFT) was stung the most, down 33% from its 2025 peak.

It wasn’t just AI casting a dark cloud over some areas of big tech. Meta Platforms (META) and Alphabet (GOOGL)—once high-fliers in the Communication Services sector—were slapped with adverse court rulings last month regarding social media’s impact on young people. META is 27% off its record high, while GOOGL is down 16%.

S&P 500: Drawdowns From 52-Week Highs

Source: Finviz

Lastly, on the tech theme, worries grow regarding how profitable AI investments will really be. NVIDIA (NVDA) closed Q1 basically unchanged from where shares traded last summer. The price-to-earnings ratio for the world’s most valuable stock is now below that of the S&P 500. Value investors may be licking their chops, but a compressed P/E is also a sentiment indicator pointing to softer fundamental trends possible in the quarters to come.

The war and AI jitters have been causes for concern. So too has private credit. We’ve been in front of this topic for many months, so we won’t do a deep dive today.

Policy, Inflation, and the Macro Backdrop

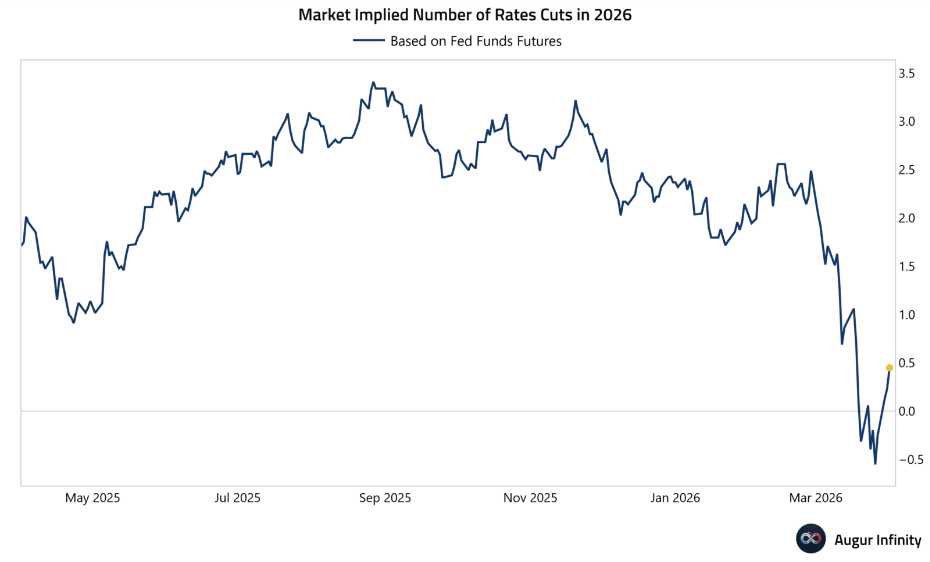

From a macro perspective, all of these risks put the Federal Reserve and other central banks around the world stuck between “Iran” and a hard place, as strategist Ed Yardeni likes to say. U.S. inflation cooled to 2.4% year over year in February but is likely to scale 3% very soon (courtesy of higher energy prices).

Fed Chair Jerome Powell offered assuring remarks at a fireside chat with Harvard University students in late March, suggesting that the Federal Open Market Committee should largely look through the oil price shock. Similar events throughout history have not been long-lasting, so a reactive rate hike may not be the FOMC’s best course of action.

Fed Rate Outlook: Small Chance of a Cut This Year

A Check on Earnings

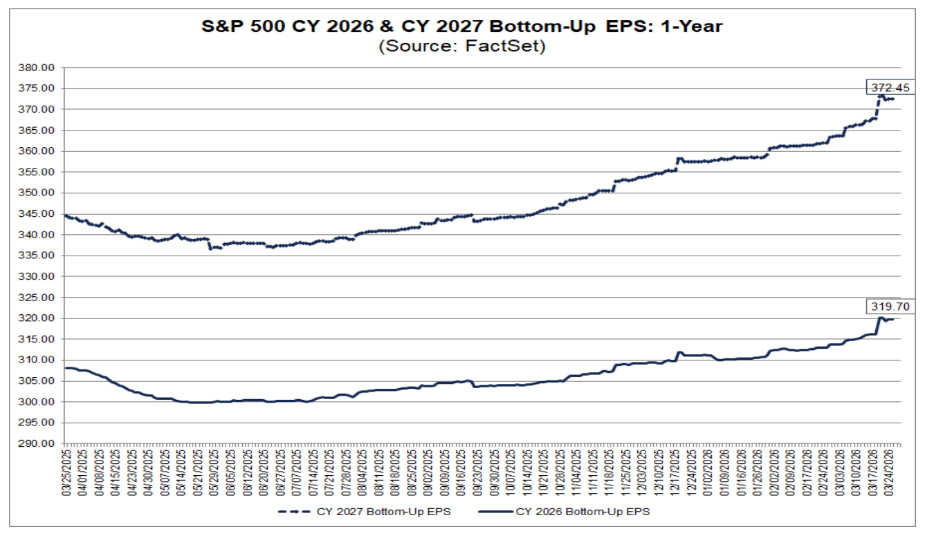

The macro foundation feels as shaky as ever compared to recent history. S&P 500 companies appear unfazed, though, at least according to the latest earnings expectations. According to FactSet, this year’s earnings-per-share forecast is up to a record-high $320. The out-year EPS estimate has also been on the rise, now up to $372.

The result is a compressed S&P 500 P/E ratio, though it’s possible that analysts will reduce their corporate profit outlooks once Q1 results are posted this month and next.

S&P 500 EPS Forecasts: Record Highs in March

The Bottom Line

Stocks and bonds fell in March. It felt like déjà vu all over again for investors, as early-2026 intermarket action was eerily similar to that of a year ago. The war in Iran, rising gas prices, AI fears, a soft labor market, and imminently higher inflation all weighed. Market watchers will soon turn to the corporate earnings season, but also with an eye on President Trump’s social media account.

Volatility lingers, but that’s not necessarily a bad thing. It can be ideal for Structured Note buyers, and the Halo team is here to help advisors craft better portfolio solutions for their clients.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and informational purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and is not intended to portray a recommendation to buy or sell a particular product or service.