What’s Ahead:

- 2023 appears to have been another record-breaking year for annuity sales, though growth could slow this year.

- Favorable demographic trends and rising cash levels are opportunities for advisors to help their clients access the growing number of annuity options.

- Halo Investing Insurance Services and our outsourced insurance desk (OID) make the process of researching, purchasing, and managing annuities simple.

Annuities continue to be a hot item among risk-conscious investors. Financial advisors find themselves needing to meet a demand surge, even after a year in which traditional stock and bond investments fared well. According to LIMRA, total annuities sales jumped 10% year over year to $88.6 billion through the third quarter of 2023. We don’t have the full-year numbers just yet, but through last September, the year-to-date sales total was tracking 21% ahead of the previous year’s pace. We will soon find out if LIMRA was accurate in its estimate for a stout 10% sales increase for all of 2023.

The Annuity Boom Presses On, Though Slower 2024 Growth Predicted

Not a whole lot has changed to cause investors to look elsewhere for protective investment solutions. LIMRA expects continued strong annuities sales amid generally improved economic conditions, aging demographics, and more guaranteed-income solutions over the coming quarters.

The group forecasts sales growth to dip this year, but then hit more record volumes in 2025. Quickly rising interest rates, currently elevated money market yields, and demand for CDs are the likely culprits for slowing annuity volumes versus the incredible growth rates seen in recent years.

Record-Low Interest Rates Left Their Mark

Looking back, the last handful of years could not have been a better time for the annuity market and retail customers. It was just three years ago when the Federal Reserve kept its foot on the monetary stimulus pedal, pumping liquidity into an economy that was already receiving hefty amounts of fiscal stimulus. Stock prices had recovered greatly from their March 2020 lows while interest rates were extremely low, still significantly under 2% throughout 2021. That setup allowed many baby boomers to lock in one final refinance on their home or move about the country to their desired retirement spot.

More Retirees and Modest Treasury Yields Fueled Interest in Annuities

On the investment front, annuities began to gain steam as record numbers of folks were leaving the workforce in the wake of the pandemic. A wave of early retirees also struck the economy, pressuring the labor force and employers who would go on to “labor hoard” as a means to ensure enough staff.

More retirees in an era of record-low interest rates meant investors had to look beyond traditional investment options to secure a decent income stream to fund their golden years. Annuities’ payout structure of investment earnings, return of original investment, and mortality credits looked better than ever – generally, the lower market interest rates are, the more an annuity’s mortality credits comprise the total payout.

Emerging Products to Meet the Needs of Today’s Investors

Indeed, annuity sales took flight starting in 2021. Volumes had fallen in 2020 to $219 billion but then rose 16% the following year to just shy of $255 billion. The pandemic’s excess savings and the overall strong financial position of so many people in their 50s, 60s, and 70s helped the annuity boom begin. Quarterly demand growth changed the industry and new providers crafted new policies.

For instance, the dearth of quality long-term-care insurance options resulted in such arider being added to some annuity types. Moreover, multiyear guaranteed annuities (MYGA) gained steam as a higher-income option compared to, say, CDs. Still, plain-vanilla fixed and deferred annuities designed to fund daily retirement spending and protect against longevity risk remained popular vehicles.

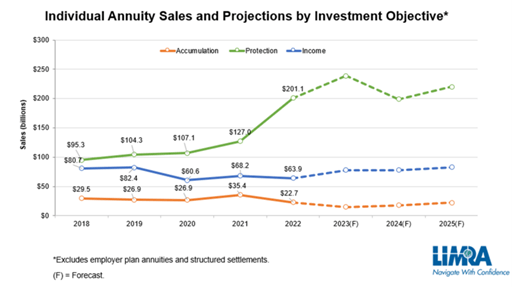

LIMRA: Annuity Sales Trends & Forecasts

Rates Finally Rise — Welcome News for Prospective Annuity Owners Amid Troubled Times for Investors

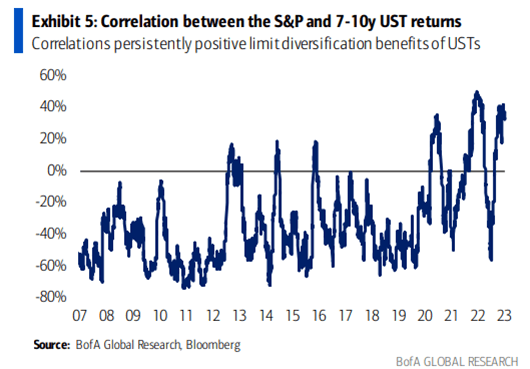

By 2022, annuity sales jumped again to $313 billion, up more than 25% annually, and rising interest rates put the spotlight on income options for risk-sensitive investors. Carriers were constantly increasing their crediting rates while volatility in the stock market prompted investors to rethink their allocations. Not only were equities falling in value, but bond investors endured unusually high volatility, too.

That year turned out to be the worst on record for the traditional 60/40 portfolio, which plunged even lower than 2008’s 14% decline. To this day, early in 2024, the correlation between stocks and bonds remains near multidecade highs, making traditional portfolios of equity and fixed-income funds riskier than was seen at times in the previous decade.

The Stock-Bond Correlation Remains High

Cash Yields Jump

Annuity demand momentum persisted through last year despite the S&P 500’s 26% total return and minor bounce back among domestic and global bonds. Household net worth levels, thanks to rallying financial and real estate markets since the pandemic, approached a new record high by the middle of 2023. There was a new twist on the retirement income landscape, though.

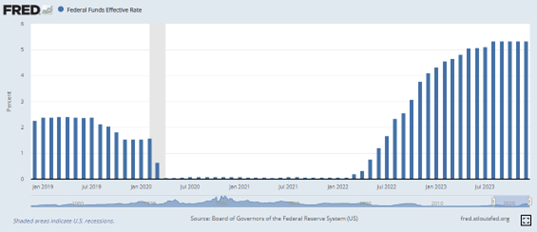

Yields available on money market mutual funds were quickly on the rise. The Federal Reserve was on a mission to clamp down on inflation. The monetary policy authorities, criticized for letting inflation get out of hand during and after the pandemic, took short-term interest rates from essentially zero to above 5% in just 15 months. The final hike, it appears, took place last July.

U.S. Federal Funds Effective Rate: Near 0% to Above 5%

Money on the Move

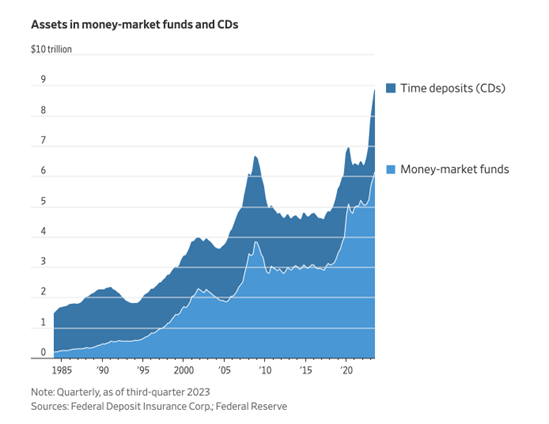

Higher interest rates of course pressured stocks and bonds, but positive real yields available in money markets and high-yield savings accounts understandably caused what is known as “cash sorting” among investors. That simply means money fled from non-interest-bearing accounts to ones that were competitive with short-term Treasury rates. What does that have to do with annuities? Well, record cash levels in money market funds also meant a massive jump in interest payments to certain segments of the investor population – high-net-worth individuals and couples and those in the age 60 and up crowd. That extra liquidity could be the fuel for the next annuity boom.

Money Market Assets Swell

What Lies Ahead

Interest rate cuts now appear imminent, according to the federal funds futures market. Given this reality, investors riding out market volatility in the perceived safety of money market mutual funds will likely see smaller annual percentage yield (APYs) very soon.

As for annuities, LIMRA predicts lower market interest rates in 2024 will lead to a temporary dip in total sales. Sluggish activity relative to recent periods may be most apparent among income-annuity products and fixed-rate deferred annuities, according to the industry group. LIMRA still forecasts a return to annual growth by 2025, though.

Digging Into Annuity Sales Trends

The future still looks bright for annuity carriers. More than three million Americans will reach typical retirement age this year. Income-annuity sales may benefit the most from this broad trend, no matter what gyrations take place in the S&P 500 and interest-rate market.

LIMRA expects income-annuity demand to surge from $15 billion in 2024 to more than $18 billion next year. Registered index-linked annuities (RILAs) appear poised for continued growth, potentially reaching five consecutive years of record sales. Finally, while regulatory uncertainties persist, traditional variable-annuity sales are seen rising 10% this year and 8% in 2025.

Advisors: Don’t Miss Out

Advisors have a lot to look forward to in the annuity space. Partnering with Halo to access this growing market can help your practice flourish. By teaming with Halo Investing Insurance Services, advisors can expand their product offering while keeping assets under their control.

Outsourcing may be the right solution as it eliminates many of the traditional annuity and insurance regulatory burdens and requirements. There are no costs or membership fees to access fee-based annuities on the Halo platform. Single premium, multiyear guaranteed, fixed index, and variable annuities are available along with RILAs.

Rethinking Risk

For many retirees, 2024 may be the year to focus on a new risk strategy. Last year’s rebound across asset classes was a welcome financial boon, but uncertainty lies ahead as the Fed prepares to reduce interest rates. Stock market valuations are back at lofty levels and the correlation between equities and fixed income is uncomfortably high.

Annuities can be an effective protective investment solution to guard against these risks. What’s more, the growing number of retirees who may have ample cash on the sidelines may earn solid returns today compared to years ago using a variety of annuity types. Advisors should not miss out on the trend, and Halo’s team is dedicated to making the transaction and lifecycle management processes smooth.

The Bottom Line

As annuities continue to be a preferred choice for risk-sensitive investors and the growing number of retirees, navigating the investment landscape presents challenges and opportunities. Annuity sales could cool off this year, but growth is forecast to snap back in 2025, offering a chance for advisors to grow their business. Wealth managers and financial planners can offer more value to new and existing clients by tapping Halo’s dedicated team of annuity professionals.

Annuities are not suitable for all investors. All recommendations for annuity products must be suitable and appropriate for the client and must be based on a thorough fact finding and understanding of the client’s unique financial situation, needs, goals, and risk tolerance.

Please see our Halo Disclosure Page for important disclosures.