What’s Ahead

New lower interest rate regime, new opportunities in structured notes

- Treasury yields were volatile in the quarters leading up to the first U.S. Federal Reserve rate cut in September.

- A large half-point ease surprised some market participants in the third quarter, and more eases are signaled by the Federal Open Market Committee’s (FOMC’s) latest dot plot.

- With short-term rates moving lower, an opportunity emerges with Steepener Notes to secure today’s term premium.

- Growth Notes tied to a new GARP equity index present an equity idea.

Much ink was spilled debating whether the Federal Reserve would begin its rate-cutting campaign with a traditional quarter-point ease, or if a jumbo 50-basis-point cut was in the works. The September 18 decision of a half-point slash to the policy rate surprised some economists, but stock and bond markets took it in stride. The U.S. Treasury rate curve continued its steepening trend, driven by buying on the short end while longer-term rates crept higher as the third quarter came to a close. The S&P 500, meanwhile, finished September at an all-time high.

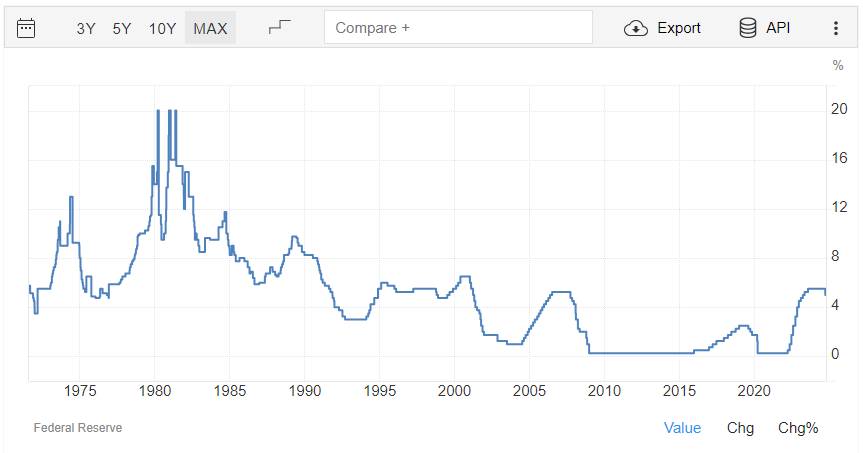

Effective Fed Funds Rate: A Rate-Cutting Cycle Is Underway

More Fed Action Expected Through the First Half of 2025

Looking ahead, bond traders price in another half point (or more) of easing this year and that could come, in part, via another jumbo cut the day after the election. Fed Chairman Powell recently remarked that the FOMC is not in a rush to bring the fed funds rate to its perceived long-term neutral rate, now at 2.9% per the latest Summary of Economic Projections (SEP). The fed funds futures market disagrees somewhat, as it prices in about 180 basis points of cuts over the next year, and economists project a terminal rate 50 basis points above current market pricing.

FOMC Fed Funds Rate Forecast (Median Values, End of Year)

Regardless of the precise policy moves, risk-sensitive investors are now in a new regime, one marked by falling short-dated Treasury yields and potentially rising rates further out on the curve. Thus, taking a proactive approach to fixed-income portfolio management may be prudent. What’s more, incorporating Structured Notes into a diversified portfolio could be an effective way to reduce overall volatility while still capturing decent market yields.

Analyzing Yield-Curve Strategies

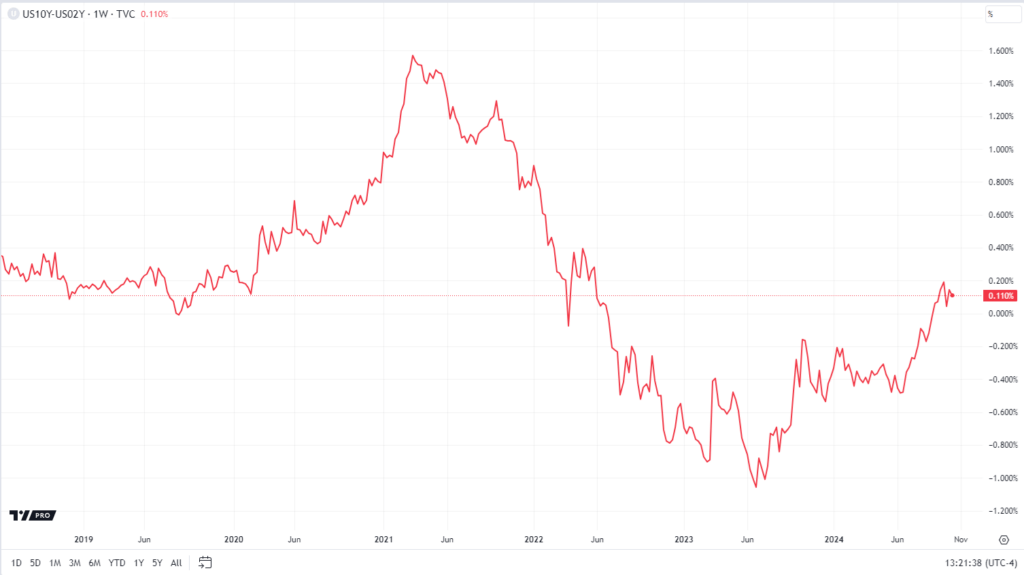

The curve steepener trade comes about in two primary ways. The first is a bull steepener, characterized by falling short-term rates. We’ve seen this play out since April, back when one last inflation scare caused investors to rethink the pace of Fed rate cuts, or even whether another hike might have been in the cards.

But the two-year Treasury note yield went on to fall from above 5% at the beginning of the second quarter to under 3.6% by the start of the fourth quarter. The “2s10s” (in bond-trader parlance) nearly printed a new cycle low toward the end of 2024’s first half, but that’s when one of the most pronounced bull steepeners began. Shortly after the September FOMC meeting, the 2s10s approached a positive 0.25%.

The second steepener type happens when intermediate- and long-term Treasury rates rise (bond selling). That’s the bear steepener, and it occurred during an equity market correction from July through late October of 2023. Rising government debt and fears regarding how long-term borrowing would be financed resulted in a temporary confidence crisis.

2-Year/10-Year Treasury Yield Spread: Steepening Ongoing Following a Record-Long Inversion

Structured Notes: A Risk Management Vehicle Amid a Shifting Bond Market

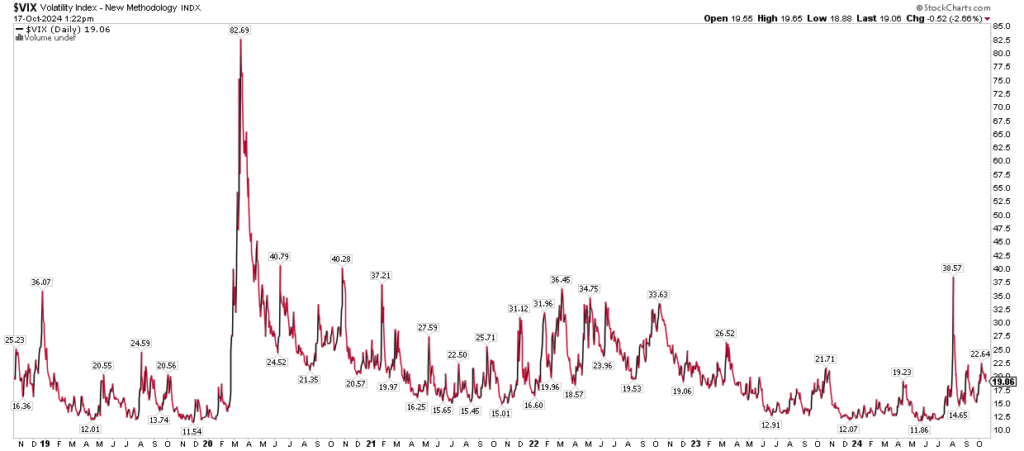

So, where does the yield curve go from here and how do Structured Notes fit in? Considering that equity volatility has remained subdued for most of 2024 (sans the early-year inflation scare and yen-carry-trade event this past August), options-based strategies could make sense heading into 2025. Another potential outcome is that the labor market stays healthy, and the 2- to 5-year section of the curve creeps up, which presents additional potential for Notes further down the line.

Such protective-investment ideas could help combat any residual policy uncertainty as a new administration takes office in Washington, and as geopolitical unrest in the Middle East shows signs of flaring up once again.

CBOE Volatility Index (VIX): Low by Historical Standards Despite Geopolitical Jitters in Early Q4

Combine the unease with suddenly lower interest rates, and Structured Notes’ yield advantage becomes all the more attractive. Furthermore, some bond market strategists assert that there remains an enduring term premium on the rate curve, suggesting that owning longer-dated fixed income through Notes could be an optimal approach to buffer against volatility.

Thus, with a slew of Fed easing on the horizon, there is a compelling case for locking in longer-term Notes today that could potentially benefit from current term premiums before further rate reductions.

Incorporating Steepener Notes

Steepener Notes can be put to work in an investor’s portfolio to prepare for a further widening between short-term and long-term interest rates. Not only is this a momentum idea, but it is also a strategy that assumes a normalization of the Treasury market. It’s possible that T-bill yields fall further while the soft-landing narrative reveals itself in the form of a higher long-bond rate.

Along with a tactical approach to portfolio management, Structured Notes offer flexibility in maturity schedules, which can help protect against reinvestment risk with existing bond holdings.

But What About Equity Strategies? Revisiting the GARP Trade

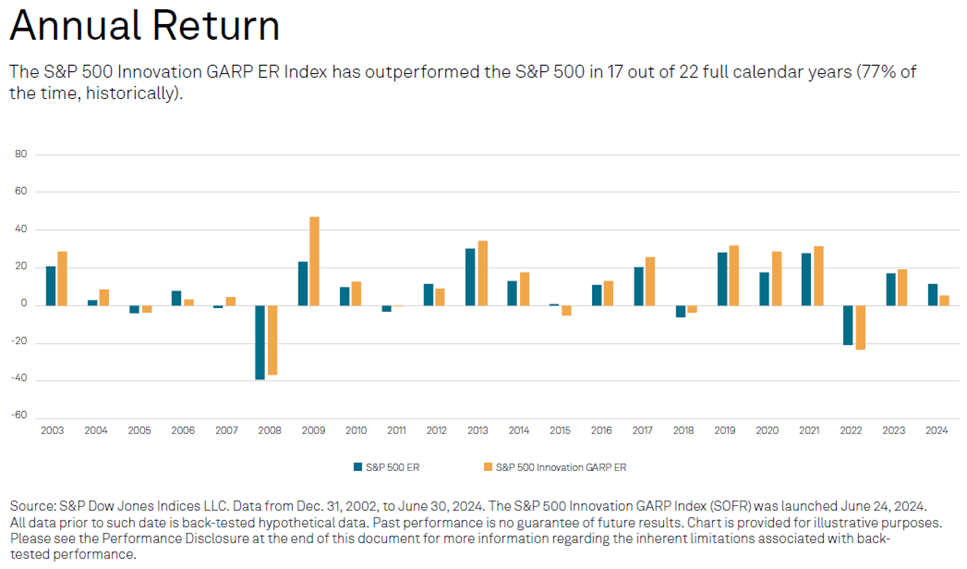

Some market prognosticators suggest that growth stocks could be a winning theme now that the rate-cutting cycle has begun. The idea is that a lower discount rate could lead to higher valuations for firms with high expected profits years into the future. The team at Goldman Sachs recently put together an S&P 500 Innovation GARP Index as they expect capital flows into equity markets given lower capitalization costs for global corporations.

Taking an all-in approach to the growth style is a risky endeavor, which is why the new index includes a value consideration. For background, GARP or “growth at a reasonable price” stocks combine factors of both growth and value. Such stocks represent companies that are expected to deliver above-average earnings growth but that are still trading at reasonable valuations compared to their long-term EPS growth rate.

A Structured Note tied to a basket of innovative technologies, including AI, blockchain, and supercomputing, is a strategy for today’s new interest rate regime and incorporates the idea of a Treasury yield curve steepener. Goldman Sachs’ underlying index applies three key filters:

- Growth: Three-year EPS and SPS growth

- Quality & Value: Free cash flow to revenue, free cash flow to debt, and earnings to price ratio

- Innovation: R&D expense as a percentage of enterprise value

Goldman Sachs S&P 500 Innovation GARP ER Index

The Bottom Line

Now may be the time to lock in longer-term Notes before additional Fed rate cuts come about. It’s clear that the FOMC wants to get back to neutral, but Chairman Powell seeks a measured approach that allows investors time to reallocate portfolios. The yield curve has gone through big swings in the past two years, and more changes between short-end and long-term Treasury rates are quite possible through 2025. Steepener and GARP Notes are ways to manage risk as fixed-income uncertainty persists while capitalizing on opportunities in the equity market.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and information purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and are not intended to portray a recommendation to buy or sell a particular product or service.

US297/1.0/2410