Key Implications:

- Some of the most popular investment products packaged by Wall Street in the last few years have been covered-call ETFs.

- Volatile stock markets and muted returns have resulted in retail flows into call-writing strategy funds.

- Structured Notes can deliver some of the same outcomes but with better risk management capabilities for advisors with clients across the risk/return spectrum..

The Great Bond Bear Market, which began in August 2020, accelerated the popularity of income-producing equity strategies. So-called covered-call funds have been around for many years, but as fixed-income returns continue to suffer amid volatile and rising interest rates, investors hungry for yield are bypassing traditional bond ETFs for stock funds that sell options on equity positions with a high dividend rate. Is this the right approach, though? Is there a better way to produce a reliable income stream? And are loftier interest rates today good enough for the average investor?

Structured Notes for Higher Yields

With many changes to the investment landscape over the past several years, these are important questions to ponder. For the unfamiliar, Structured Notes could make a better alternative for investors seeking elevated investment-income generation, but who also want the assurance of some principal protection.

Along with delivering similar return characteristics as call-writing funds, advisors using Notes have the potential to more effectively manage and tailor client portfolios.

The Scarcity Effect:

Fewer Income Options Drive Flows

Taking a step back, the proliferation of covered-call ETFs began not with the bond bear market that started in 2020, but with the zero-interest-rate era of the 2010s. The Federal Reserve suppressed short-term interest rates and occasionally conducted monetary policy operations to pressure yields further out on the curve.

This presented a significant challenge for baby boomers, who began retiring in droves, shortly after the Great Financial Crisis. No longer could these risk-sensitive investors park cash in money markets or CDs and earn a safe yield to meet their daily spending needs. Indeed, the rate on Treasury Inflation-Protected Securities (TIPS) plunged from about 4% at the turn of the century to near –1% by 2012. Despite an increase in Treasury yields through 2018, the real return on these fixed-income investments only briefly topped 1% before all-time lows were set in 2020.

TIPS Yields Crater to Historic Lows in the 2010s and Early 2020s

Want Yield? Take More Risk.

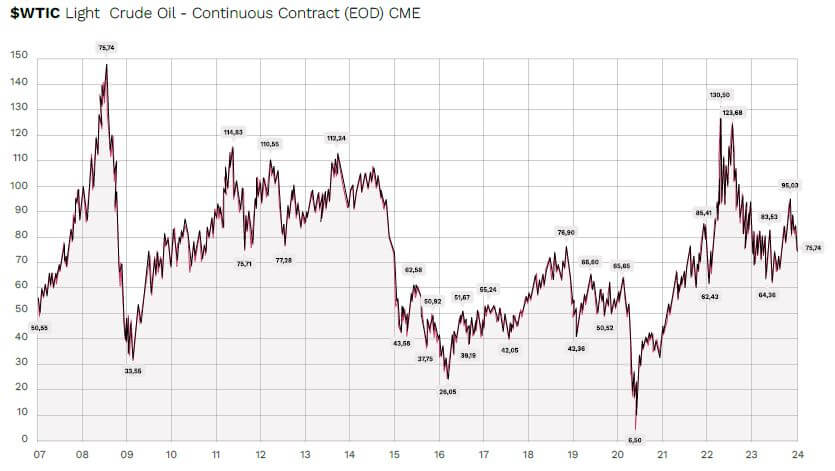

So, for much of the 2010s, conservative investors had to step out on the risk curve to ensure their nest eggs would endure. You might recall that Master Limited Partnerships (MLPs) were a popular place to overweight a portfolio in the chase for high income, but the oil crash of 2014 through early 2016 sent unit prices of those partnerships plummeting – the income earned over the course of a year was often wiped out in just a handful of poor trading days. Domestic oil prices plunged from over $100 per barrel to under $30. A recovery rally in some Energy-sector stocks helped investors who took that bet, but oil’s historic free fall into negative territory may have been the death knell for that income-producing strategy.

Volatile Oil Prices and Fluctuating Energy-Demand Trends Stymie MLP Interest

The Wall Street Machine Kicks Into High Gear

As historically low Treasury yields and once dependable equity-dividend-yield portfolio methods failed to deliver reasonable income returns for the growing retiree population, Wall Street got crafty. Options trading had already been on the rise as the last decade progressed. Meanwhile, better technology and rising trading volumes brought down transaction costs in derivatives markets. Moreover, the backing of major exchanges and clearinghouses instilled confidence in those markets even during periods of spiking volatility. The conditions were finally ideal for covered-call ETFs to rise to prominence.

Covered-Call ETFs: What Are They?

For background, covered-call funds employ options strategies, such as writing slightly out-of-the-money calls to generate an income return on top of the return of the performance of underlying securities. The covered-call strategy offers a form of downside protection – by receiving premiums from writing call options, the ETF’s high distribution rate can partially cushion potential losses in a fund’s underlying stock holdings.

Today, you’ll find no shortage of such products featuring, in some cases, double-digit yields. Also making these ETFs intriguing to prospective investors is that volatility metrics appear favorable compared to the broad-market index ETFs. A strong reported yield, some price appreciation, and relatively modest volatility? What’s not to love, right?

Big Growth Amid Sideways Stock Markets

Some of the fastest-growing ETFs are in this category, and new strategies are launched seemingly each week. Growth has exploded so fast that fund providers have created single-stock, covered-call ETFs that simply target one high-profile company, and craft a synthetic portfolio using derivatives to mimic the return of a covered-call play on an individual stock.

Is the playing field getting too crowded with too many options (pardon the pun)? That’s debatable, but there is no doubt that the recent stretch has been nearly the perfect setup for covered-call ETFs to flourish. When bear markets strike and volatility runs consistently above average, this income-producing strategy can work wonders.

The Major ETF Players

The Global X Nasdaq 100 Call ETF (QYLD), while not the largest in its category, has traded for 10 years. Returns compared to the Nasdaq 100 have not been particularly impressive leading up to the market peak in early 2022. A multiyear bull market in large tech stocks meant that selling upside calls simply gave away gains to investors who were long the equities outright – as the fund was forced to pay the option buyer the difference between

the stock price and strike price when the underlying equity rallied through a call option’s strike price. Since the Nasdaq 100 peaked, though, QYLD has outperformed much of the time with significantly less volatility.

Elsewhere, new money has poured into the JPMorgan Equity Premium Income ETF (JEPI) since its launch in May 2020. JEPI is a more broad-based ETF, generally holding low-volatility stocks with a value-based construction methodology. Popularity was so strong early on that it set the annual record for active ETF inflows in 2022 with more than $12 billion, according to Bloomberg’s Eric Balchunas. AUM is now near $30 billion, making JEPI the largest actively managed ETF, Morningstar reports. The ETF Store’s Nate Geraci notes that JEPI has taken in roughly $13 billion in new money through October 2023 despite trailing the S&P 500 in total return by some 11 percentage points. Underscoring the JEPI fervor, since the ETF’s inception, $31 billion has flowed into the fund all while the strategy has underperformed the S&P 500 by 10 percentage points.

Covered-Call ETFs Boasted Big Relative Returns During the 2022 Bear Market

These nontraditional funds are all the rage with retail investors. In 2022, QYLD fell 19%, with dividends included, far less than the Nasdaq 100’s 32% decline. JEPI meanwhile returned just -3.5%, easily beating the S&P 500’s 18% loss. Quarterly fund inflows continue to be stout – perhaps driven by ongoing shakiness in equities and recency bias at play among active investors.

Sideways stock market action with elevated volatility means higher income from selling calls and fewer instances of being effectively called away on positions. A key risk looking ahead, however, is if we see another significant leg to this bear market or if a new bull run is already underway. In both of these “trending” market scenarios, investors who have recently piled into covered-call ETFs could be in a perilous position.

Structured Notes: Upside Exposure, Downside Protection, Effective Portfolio Management

We believe that Structured Notes can make a better alternative. The allure of covered-call writing strategies certainly capitalizes on investors’ proclivity for yield, but as more money piles in, there’s the risk that retail investors could get caught flat-footed during the next market cycle. With characteristics similar to those of covered-call ETFs, Structured Notes have the potential to attract investors.. Let’s outline how Notes can be used from a portfolio perspective and what types of investors might be well served owning them.

Structured Notes have something broad ETFs cannot offer – customization. A hybrid vehicle between stocks and bonds on the efficient frontier, advisors teaming with Halo can create Notes based on the unique risk tolerances and return objectives of their clients. Personalization often creates buy-in from investors, helping them stick to a strategy during both frothy bull markets and discouraging bear markets. There are several levers the advisor can pull to craft a Note, such as the maturity date, underlying asset, downside protection level, and return/payoff profiles. In that sense, Notes are like the Swiss Army Knife of investing, not some blunt income-generating tool.

Growth and Income Notes:

Tools to Build Better Portfolios

Along with customization benefits, we find that clients are attracted to Notes’ principal protection feature. Similar to how covered-call strategies can work in sideways to slightly-negative markets, Note investors can get their principal fully returned to them even if the underlying asset exhibits mediocre performance. Along the way, an enhanced yield generates a high income return – potentially well above the interest rates on Treasuries and corporate bonds.

Structured Note Types: Risk & Return

Growth Notes offered through the Halo Marketplace feature enhanced upside exposure. Unlike defensive covered-call strategies, Growth Notes can be owned by investors concerned about missing out on a new bull market. Halo’s Hedged Equity Strategy details how Notes can be used to construct a better risk-managed portfolio. As for Income Notes, they can be owned to mitigate a host of market risks that income-focused ETFs fail to protect against.

Scenario 1:

Early Retirement Protection

For example, let’s say an advisor has a newly retired couple concerned about sequence-of-return risk. The first handful of years without a paycheck can be financially stressful, so constructing a temporarily defensive allocation that generates income and has downside risk protection is important.

Income Notes with targeted maturity dates and Hard Protection could make an interesting alternative to covered-call strategies. Ideally, as the couple’s portfolio grows without significantly tapping into principal, the Income Notes mature and can be reinvested in Growth Notes – this is akin to Michael Kitces’ Bond Tent strategy. The transition essentially goes from receiving a conservative fixed return via periodic coupon payments to having upside participation on an underlying asset or index.

Scenario 2:

Capturing Bull Market Returns Through Dynamic Asset Allocation

In another instance, with an active investment-management approach, Growth Notes could be put to work to capture enhanced upside equity participation. Years like 2013 and 2017 – periods of rising stock prices and low volatility – were awful stretches for owning covered calls, resulting in significant underperformance. Using Structured Notes, though, a holder could have earned outsized returns with an Uncapped Enhanced Participation

Growth Note.

Managing Plans & Portfolios Using Structured Notes

As you can see, a wide range of investor types can benefit from Structured Notes. What’s more, advisors looking to act upon a certain market outlook may also use Notes to accomplish their goal. This degree of customization cannot be achieved with covered-call ETFs. Notes, like call-writing strategies, also offer the general characteristics of lower-risk market exposure (compared to index ETFs) with an elevated yield.

The Bottom Line

Covered-call ETFs continue to be popular among everyday investors. The allure of high-income returns along with lower volatility versus the overall stock market is no doubt powerful. Structured Notes may be a better alternative for advisors seeking to manage customized portfolios for their clients. Both aggressive Growth Notes and more defensive Income Notes can be put to work for investors spanning risk tolerances and return objectives, all while providing a solid income stream.

Please see our Halo Disclosure Page for important disclosures.

The information provided here is neither tax nor legal advice and should not be relied on as such. Investment involves risk including possible loss of principal.

FOR INSTITUTIONAL, FINANCIAL PROFESSIONAL, PROFESSIONAL INVESTORS, AND WHOLESALE INVESTOR USE ONLY. This communication should not be distributed, in its current form, to end-investors, and it is for investment professionals only.

The material is for information purposes only. It is not intended for and should not be distributed to, or relied upon by, members of the public.

It is not intended to be a forecast, research or investment advice, and is not a recommendation, or an offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are subject to change. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations. Reliance upon information in this material is at the sole risk and discretion of the reader. The material was prepared without regard to specific objectives, financial situation or needs of any investor.

Past performance is not a reliable indicator of current or future results.