Headquarters Office Building in Washington, D.C.")

What’s Ahead:

- A divided Fed and leadership transition could keep markets volatile well into the new year.

- Private credit faces mounting risks amid uncertain financial conditions and rising competition in the bond market.

- Investors may want to consider protective investment strategies to manage risk in 2026.

Grab your popcorn. It’s shaping up to be an action-packed year of Fed watching. With a new chair set to take the helm of the Federal Open Market Committee (FOMC) and an uncertain macro backdrop, every piece of “Fed speak” and major economic data release will be closely scrutinized.

The Fed meets this month on the 27th and 28th. It will presumably mark Governor Stephen Miran’s final appearance, while a fresh batch of regional Fed presidents will cast votes.

A Look Back at the 2025 Fed Policy Pivot

Recall that last year, the FOMC cut its policy rate three times in what were widely viewed as “emergency cuts.” The economy was not falling off a cliff, but emerging downside risks to the jobs market prompted a dovish pivot. Stocks and bonds rose when Chair Jerome Powell intimated that the rate-cutting cycle would resume in September, speaking from the familiar confines of Jackson Hole, Wyoming.

Powell’s annual address, delivered beneath the shadows of the Grand Tetons, came just three weeks after a stunningly weak July jobs report—one that led President Trump to call for the removal of the head of the Bureau of Labor Statistics.

That same afternoon, Fed Governor Adriana Kugler announced her resignation from the Federal Reserve Board for reasons that were unclear at the time. We now know she and her spouse were involved in repeated violations of Fed trading rules.

Adding to the drama, Governor Lisa Cook faced allegations of mortgage fraud leveled by the president. While Dr. Cook may remain on the Board, the episode further fueled political tensions surrounding the Fed.

The “Apprentice” Comes to the Eccles Building

The monetary policy soap opera took a deeper twist as year-end 2025 approached, with a real-life version of “The Apprentice” playing out in public view. Three men emerged as finalists to succeed Powell as Fed chair. Colloquially dubbed “the two Kevins,” Kevin Hassett and Kevin Warsh were widely seen as front-runners. Hassett is an economist serving as director of the National Economic Council since 2025, while Warsh is a banker who previously served on the Federal Reserve Board of Governors from 2006 to 2011.

The third contender, Chris Waller, is a current Fed voting member. His macroeconomic predictions have largely come to pass, earning him respect among economists and Fed watchers alike.

A Divided Fed Faces a Steep Learning Curve

Whoever President Trump selects will face an uphill climb beginning May 16. The 17th chair of the Federal Reserve must quickly earn credibility and consensus among the other 18 FOMC members. The Fed enters the year deeply divided, with hawks and doves firmly entrenched. Many observers argue that political ideology has increasingly seeped into the halls of the Eccles Building in Washington, D.C.

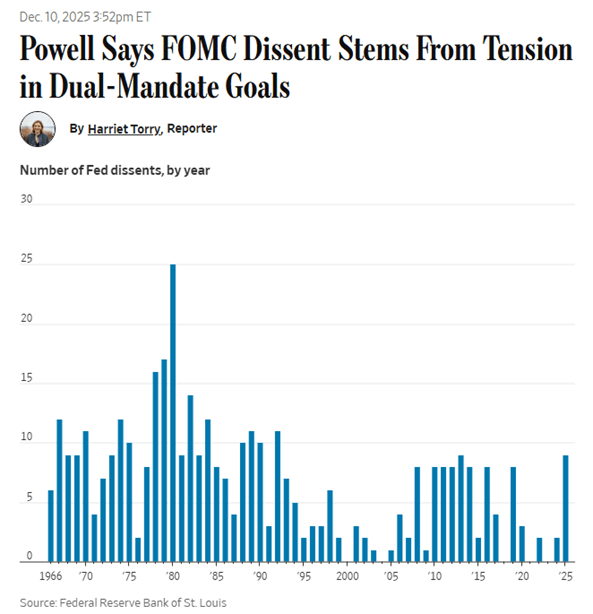

At the December meeting, three dissenting votes undercut the ultimate decision to cut rates by a quarter point for the third consecutive time. Kansas City Fed President Jeff Schmid and Chicago Fed President Austan Goolsbee voted to hold rates steady, while Miran — a Trump loyalist — voted for a jumbo half-point cut.

Disparate Monetary Policy Views at the Fed

Calling for Consensus

Powell, as part of his legacy, effectively herded the cats in December. Other hawks on the FOMC likely cast reluctant votes to ease policy. Still, enough consensus emerged to bring the Effective Federal Funds Rate down to a 3.5%–3.75% range by the end of the year.

Volatility Driven by Policy Signals

It is now reasonable to expect additional Fed-induced volatility across stock and bond markets. The fourth quarter was marked by notable swings, largely driven by speculation over the policy path.

Powell cooled bullish sentiment during his late-October press conference, only to see it reversed by dovish remarks from New York Fed President John Williams (often viewed as the FOMC’s second-in-command) just before Thanksgiving. Williams effectively teed up a December cut, which ultimately materialized.

The public doesn’t know for sure, but it’s speculated that Powell OK’d William’s comments in advance. The New York Fed president’s reassuring words were all the bulls on Wall Street needed to send the S&P 500 to a new record high. But renewed AI worries and rising long-term interest rates then cooled the fervor heading into Christmas.

What It Means for Investors

Volatility may be here to stay, particularly as it relates to the Fed’s influence on markets. The very end of 2025 was anything but merry for the S&P 500 and the benchmark 10-year Treasury yield.

Ongoing uncertainty around inflation, growth, and interest rates could also pressure a fast-growing corner of the investable universe in 2026: private credit.

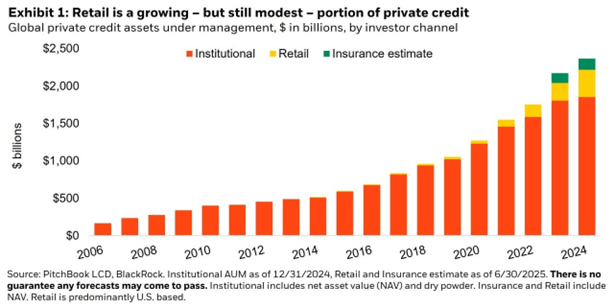

Understanding the Private Credit Boom

Private credit can be thought of as an alternative to public bond markets or traditional bank loans. In its simplest form, it involves non-bank institutions lending directly to companies. Because these loans are not traded on public exchanges, they are considered private.

The space has expanded rapidly, with assets under management nearing $2.5 trillion, up from just over $500 billion a decade ago. Toward the end of 2025, however, cracks began to appear.

In October, bad loans and allegations of fraud involving First Brands and Tricolor were not directly tied to private credit, but JPMorgan Chase CEO Jamie Dimon referred to them as “cockroaches” — a potential warning sign of broader stress in lending markets.

The Private Credit Boom: Near $2.5 Trillion Invested

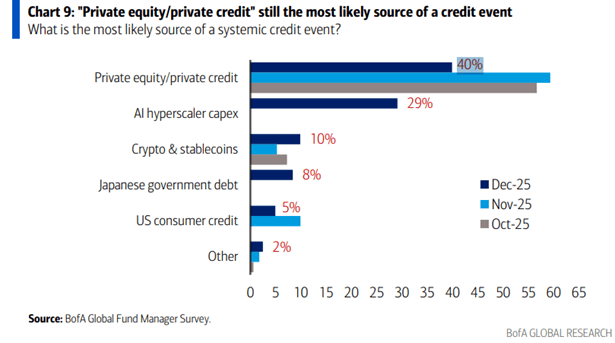

Opacity and Structural Risks

Private credit is inherently opaque. These loans are generally less regulated than traditional corporate bonds, leaving investors with limited insight into borrower fundamentals. “Zombie” companies — firms that generate just enough cash to service interest payments — frequently tap private credit markets.

At the same time, as competition among lenders intensifies, covenants are often weakened or removed, reducing investor protections if borrowers stumble. Not surprisingly, portfolio managers deemed private credit as the most likely source of a systemic credit event, according to the December Bank of America Global Fund Manager Survey.

Private Credit Seen as the Most Likely Source of Systemic Credit Risk

Where the Fed Fits In

If financial conditions tighten, private credit may be among the first areas to feel strain. A weaker macro environment could lead to more defaults and markdowns. Complicating matters, private credit assets are not valued as frequently as public bonds, meaning price declines can appear suddenly.

Loans can move from near par (full value) to deeply discounted with little warning. Whether the next Fed chair will be tested by stresses in private credit remains an open question.

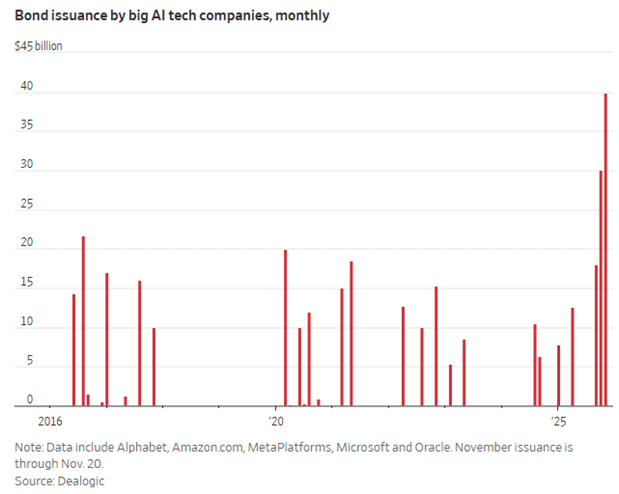

Supply, Demand, and a New Competitive Threat

Another force reshaping fixed income is basic supply and demand. Fueled by the artificial intelligence boom, technology companies are increasingly turning to public bond markets to finance investments.

Some analysts expect 2026 to be a record year for investment-grade bond issuance. If investors can access higher yields in liquid, transparent public bonds, private credit may lose some of its relative appeal.

WSJ: Flood of AI Bonds Adds to Pressure on Markets

Where Protective Investment Solutions Come In

Against this backdrop of Fed uncertainty, valuation risk, and opaque credit exposures, investors may look for ways to remain allocated while managing downside risk. This is where protective investment solutions, such as Structured Notes, can become part of the conversation between advisors and clients.

Competitively priced Structured Notes may offer defined outcomes, including downside buffers or capital protection features, while still providing exposure to equity or rate-linked opportunities. However, these features are subject to the credit risk of the issuer, meaning if the underlying financial institution fails, investors may lose their principal regardless of any built-in protections. For investors wary of sudden repricing or limited transparency, Notes can introduce a more rules-based approach (with defined outcomes) to risk management and clients’ portfolio allocations.

Structured Notes are not a cure-all, and they come with their own nuances, but in an environment marked by policy-driven volatility and evolving private credit risks, their customizable payoff profiles may appeal to everyday investors seeking balance between participation and protection.

The Bottom Line

A new Fed chair, persistent volatility, and mounting questions around private credit suggest risk management will likely remain front and center. In uncertain markets, clarity around exposure and downside may matter as much as the pursuit of returns.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and informational purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and is not intended to portray a recommendation to buy or sell a particular product or service.

US405/1.0/2601