What’s Ahead:

- Strong market rallies often cause nervous investors to sell early, and buffered ETFs do them no favors.

- Structured Note strategies from NewEdge Investment Solutions harness the expertise of experienced portfolio managers.

- Buffered ETFs face many constraints, resulting in the risk of suboptimal allocations for advisors and their clients.

The stock market returns about 9% per year on average. The last two words there are the key qualifiers. The truth is, few years actually realize the 6-10% so-called “typical” return; there are fat performance tails that make trying to time the market extremely challenging, even for seasoned investors. Today, we aren’t going to deride market timers. Rather, we aim to underscore the perils of continuously capping potential gains via static products like defined outcome or buffered ETFs.

Buffered ETFs have quickly gained traction in recent years among financial advisors seeking to offer their clients downside protection. But this strategy comes at the cost of surrendering potentially significant gains. It’s a defined-outcome strategy that can work in some situations, but there’s a better way to implement protective investment solutions in client portfolios.

Structured Note strategies implemented via SMAs, such as the NewEdge Investment Solutions Structured Note Advisory Portfolio (SNAP) and Structured Note Income Portfolio (SNIP), can be much more effective vehicles for helping clients grow their wealth and generate income. SNAP focuses on generating equity-market-like returns with downside protection, while SNIP targets income generation, offering an alternative to other nontraditional sources of income such as private credit, but with potentially more attractive risk-adjusted performance.These professionally managed strategies offer customization, dynamic payoff structures, and flexibility to maximize gains while keeping a close eye on downside risk. Let’s compare buffered ETFs to SNAP and SNIP from the standpoint of wealth creation, not just wealth preservation. It is a different spin, but amid resilient markets in recent years, investors must not discount all that could go right in equities (case in point: 2025).

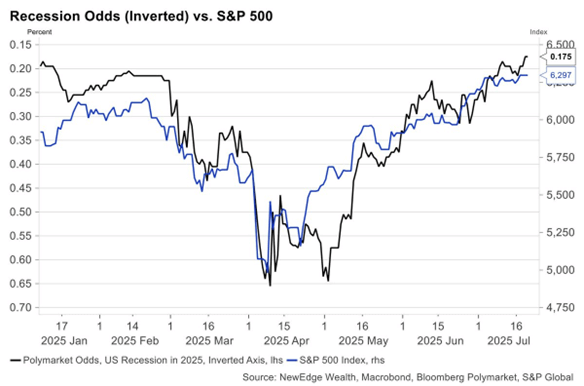

2025: A Stunning S&P 500 Rally as Recession Fears Wane

Structured Note SMAs: Upside Participation—Without the Cap

Buffered ETFs offer seemingly straightforward, exchange-traded access to defined outcome strategies. Designed to provide partial downside protection, typically buffering the first 10-30% of losses over a set outcome period (often one year), risk-conscious investors have flocked to this niche ETF type. But those who allocated heavily into them from an equity sleeve over the past few years are likely disappointed by their total returns.

The reason is the systematic risk-return trade-off. Buffered ETFs, which commonly cap gains at 10% from the ETF’s inception, can be beneficial during steady markets, but in strong rallies, significant gains are potentially left on the table, particularly for investors who buy into a buffered ETF mid-period. The products operate on a programmatic, “set-and-forget” model, typically resetting and reinvesting annually at the start of a predefined outcome period. This mechanical approach doesn’t consider market conditions, including spikes in volatility and wash-out events that can impact the risk-return construct.

Structured Notes, by contrast, are not off-the-shelf products. Professional portfolio managers at NewEdge can hand-select Structured Note terms and features such as participation rates and buffer levels to take advantage of transitory tactical opportunities.

Flexible Protection Features

Buying buffered ETFs means committing dollars to set constraints, which may include centering on hard protection. Hard protection (the buffer) can cushion the downside, but the cost is potentially reduced gains if equity markets rally strongly.

Depending on the market environment and outlook from NewEdge’s portfolio managers, there could be a preference for soft protection. While soft protection opens the door to greater losses if a dramatic market decline ensues, it also raises return potential during a strong up market. Conversely, buffered ETFs lock investors into possibly suboptimal positions for the duration of an outcome period.

Another active tactic SNAP and SNIP can claim (that buffered ETFs cannot) is the time-tested laddering method. While exchange-traded products impose caps on upside returns, SMAs can strategically stagger maturities to capture additional upside when market conditions improve, such as when signs of an equity bottom emerge.

So, the risk-return profile is more like a dimmer than a light switch with SNAP and SNIP. This flexibility allows NewEdge to be more opportunistic. Moreover, advisors can select SNAP, which uses more Growth Notes, for their more aggressive clients or SNIP, which is more Income-Note focused, for risk-averse clients.

Custom Notes Versus Standard Options

Digging further into the construction of buffered ETFs and professionally managed Structured Notes strategies, there are limitations at the foundational level with the former. They rely on standardized FLEX Options, which are typically customized only annually and offer limited flexibility in terms of structure and notional amounts. Parking client assets in such a confined strategy fails to adapt to evolving markets, and maybe more importantly, changes in a client’s personal situation and investment requirements.

Not true for SNAP and SNIP. Portfolio managers have the meaningful freedom to customize the terms, types, and notional amounts of Structured Notes, aligning individual positions with both macro- and microeconomic conditions. For advisors and their clients, this means they can benefit from either a higher-risk, higher-return vehicle with SNAP or a lower-risk, lower-return strategy like SNIP.

SNAP could allocate more capital to Structured Notes with higher uncapped upside or adjust strike levels to capture more stock-market gains. SNIP’s managers, meanwhile, might procure Income Notes with higher coupon rates. If expected market returns decline, the focus can shift back toward protection over appreciation.

Those FLEX options we mentioned earlier cannot pounce like SNAP and SNIP. Also, keep in mind that ETFs trade as a unit, so individual holdings or exposures cannot be added or removed with ease as they can with strategies implemented in SMAs.

Final Thought on Liquidity

From the viewpoint of maximizing upside returns, the perceived liquidity benefit of buffered ETFs could actually work against retail investors. Consider this scenario: The S&P 500 breaks to new highs after a long consolidation period. A nervous investor thinking there may be a significant decline might pressure their advisor to sell the ETF.

Professionally managed Structured Note strategies help to mitigate the risk of an itchy trigger finger. Investors know they are in an expertly managed portfolio, not an in-and-out product like a buffered ETF. Hence, buffered ETFs’ so-called liquidity advantage may be a cost, not a benefit, particularly when clients likely already hold securities and cash that satisfy such needs.

The Bottom Line

NewEdge’s SNAP and SNIP Structured Note strategies can be more effective tools for growing client wealth than buffered ETFs. The focus on these protective investment solutions is usually on what could go wrong in markets, but we flipped the script today.

The SMAs’ expert portfolio managers have the tools and flexibility to adapt to macro market conditions, whereas buffered funds are static, forcing investors into a predefined strategy that may be suboptimal at times.

With SNAP and SNIP, clients can better reach their goals by staying invested.

Please see our Halo Disclosure Page for important disclosures

An investment in Structured Notes may not be suitable for all investors. These investments involve substantial risks. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Content and any tools discussed are provided for educational and informational purposes only. Halo Investing makes no investment recommendations and does not provide financial, tax, or legal advice. Any structured product or financial security discussed is for illustrative purposes only and is not intended to portray a recommendation to buy or sell a particular product or service.

US388/1.0/2510