Many investors are surprised to learn that classic asset-class-based diversification isn’t the only way to reduce a portfolio’s risk. In fact at times, asset diversification produces a rather weak hedge against risk.

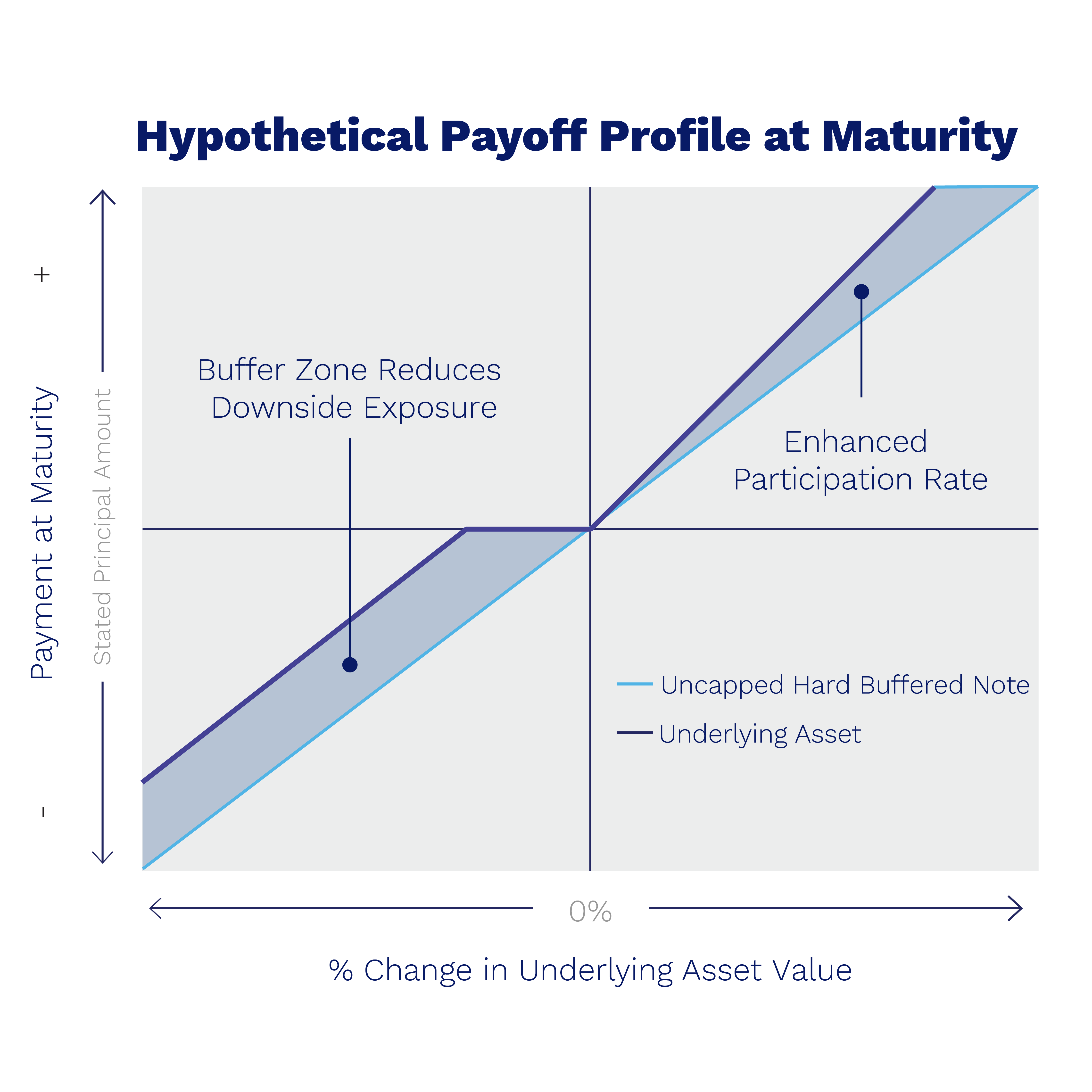

A structured note’s performance, on the other hand, is a modification of another asset’s performance. Commonly, a structured note alters both the upside potential and downside risk elements of an underlying asset. Through these adjustments, investors can potentially earn better returns with less volatility.

Without structured notes, there are two ways to decrease risk, but each features certain portfolio trade-offs.

- Allocate to lower-risk securities, potentially sacrificing return potential.

- Allocate to uncorrelated securities, potentially introducing new risks.

A chart illustrates the point. The efficient frontier below shows how a structured note with downside protection and enhanced upside participation on an underlying asset may be able to help shift an asset class’s payoff profile to a higher return and lower risk profile.

Structured notes, when incorporated into a traditional portfolio of equities and fixed-income assets, can thus mitigate some risk without giving up expected return or taking on additional beta risk.

Diversification does not protect an investor from market risk and does not ensure a profit.

Please see our Halo Disclaimer for other important disclosures.