What’s Ahead:

- Investment vehicle diversification is the next step forward to help protect client portfolios in a new market regime of correlated and volatile stock and bond markets.

- The 60/40 allocation may face troubled times ahead, but we outline ways which may better protect retirement plans.

- Structured notes and annuities can be put to work by advisors along with tax optimization strategies to enhance a client’s income stream and reduce longevity risk.

Industry giant BlackRock recently doubled down on its recommendation that investors abandon the traditional 60/40 stock and bond allocation. In a new era of higher interest rates, stubborn inflation, and volatility across asset classes, better allocation methods are needed to help ensure retail investors can reach their financial goals with confidence.

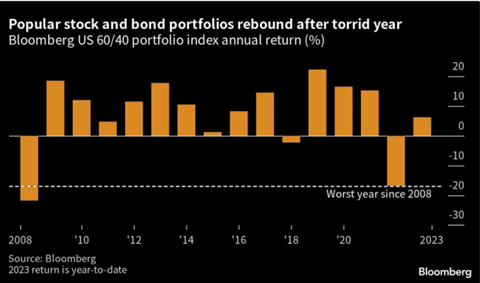

However, some would argue that the psychological damage has already been done. Consider that in 2022, the Bloomberg US 60/40 Index endured its steepest annual loss since 2008. Adjusted for inflation, last year’s -18% total return was marginally worse than what we all experienced in ‘08.

A Bounce Back for the 60/40, but Will It Last?

Rethinking Asset Allocation

It’s not just recency bias that has the world’s largest asset manager suggesting that investors break up traditional asset allocation strategies. A shift away from typical broad investments in stock and bond indexes may be required to effectively manage risk and capture a steadier long-term rate of return. BlackRock contends that aggressive monetary policy from central banks around the world is a far cry from the easy money regime of the 2010s, in which a zero-interest-rate policy led to a boom across equities and fixed income.

Stocks and Bonds Recover From Sharp Declines

So far in 2023, investors have caught a reprieve, however. Bonds have been bid as recession fears loom while mega-cap stocks have led the S&P 500 higher. While the 60/40 allocation is having a snapback from the lows notched in the fourth quarter of 2022, strategists at BlackRock caution that robust returns over recent months may not persist.

Is a More Active Strategy Required Today?

So, what is the play? Is it all bad news? Do we just have to accept lower capital market returns going forward? Maybe not. On the equity side, tactical plays to capture the upside of in-favor sectors that can withstand an economic growth slowdown might buffer against downside risk.

What’s more, the fixed income side of the ledger needs to be adjusted to account for the new reality that bonds and stocks are moving together at a rate not seen since the mid-90s. Inflation-linked bonds could work along with taking advantage of elevated short-term Treasury yields.

Are There Other Methods by Which Advisors Can Increase a Retiree’s Odds of Success?

There are broad portfolio strategies advisors and retail investors can execute in this new regime, such as diversifying among asset classes and targeting niches that could outperform. Yet there are possible perils to timing those buy-and-sell decisions, too. Another option is to think “bigger picture” by diversifying among investment vehicles, not just classes. Going beyond simple asset allocation strategies, we assert, can be a more viable approach to truly sidestep volatile stock and bond markets.

Investment Vehicle Diversification Using Structured Notes and Annuities

Annuities and structured notes are tools that advisors can leverage to craft tailored portfolios that are not as reliant on the uncertain and correlated performances of the equity and fixed-income markets. Additionally, Americans are increasingly concerned about outliving their assets, and both of these investment vehicles help mitigate longevity risk. Technology and competition have reduced the costs to acquire and own annuities and notes over the past several years, so getting creative with portfolio construction is more practical than ever.

Protective Investments Feature Withdrawal Flexibility

Annuities and structured notes are effective during the distribution stage of retirement investing as well. The guaranteed income from annuities and enhanced yields from structured notes help guard against both longevity risk and the chance that a traditional allocation may suffer another protracted downturn. Incorporating protective investment strategies can improve a client’s probability of success (that is, not running out of money in retirement).

Hedging Your Risks Through Reallocation

By reallocating, an advisor can swap a slice of a low-yielding bond sleeve from a portfolio and reposition it in structured notes that focus on generating income. That move increases the average yield on the bond portion. At the same time, part of the stock allocation can be retooled for a position in growth notes that participate in the market’s upside, while offering a layer of downside risk protection. At Halo, we have detailed a Hedged Equity Strategy that layers structured notes on top of a portfolio of stocks, bonds, and alternative investments, thereby improving the risk-return potential of an allocation.

Annuities: A Vehicle for Diversification

Annuities can help improve a client’s probability of success, too. We all know that encouraging a retired couple to cut back on their spending or consider rejoining the workforce are not pleasant conversations. Instead of those undesired lifestyle changes, portfolio adjustments designed to make an asset base last longer instill client optimism. Guaranteed cash inflows that meet and exceed the monthly expenses of a married couple in retirement is the goal. And advisors can do that through certain annuity types.

Case Study: RILAs and Roth Conversions to Craft an Enduring Income Stream

For instance, a registered index-linked annuity (RILA) used alongside a Roth conversion strategy has the potential to produce a tax-free income stream that can last decades. Suppose a client has a $500,000 Traditional IRA. She is 58 years old and recently retired. A $200,000 RILA that offers an increasing annual payout can be used in conjunction with a Roth conversion plan done within the RILA.

Adding the RILA as a new investment vehicle allows the advisor to convert, say, $50,000 per year from age 58 to 63 within the annuity. That may reduce overall taxes since the client can distribute the Roth portion of the RILA. Moreover, there may be other benefits to this type of strategy, such as lower Medicare premiums and more flexible withdrawal options throughout retirement.

The Bottom Line

Diversification beyond asset classes is needed in this new market environment. Correlated stock and bond markets, periodic bouts of volatility that shake investors’ confidence, and uncertainty regarding where interest rates may go all cast doubt on the efficacy of the 60/40 portfolio.

Spreading assets across investment vehicles – namely structured notes and annuities – can increase an allocation’s yield while reducing longevity risk. These protective investment solutions are also flexible with tax benefits, so advisors can craft strategies based on their clients’ unique circumstances and goals.